Swiggy Valuation Reveals an Expensive Lesson in Being Second

In India’s food delivery duopoly, it seems being second to market comes with a hefty price tag: a 35-40% valuation discount.

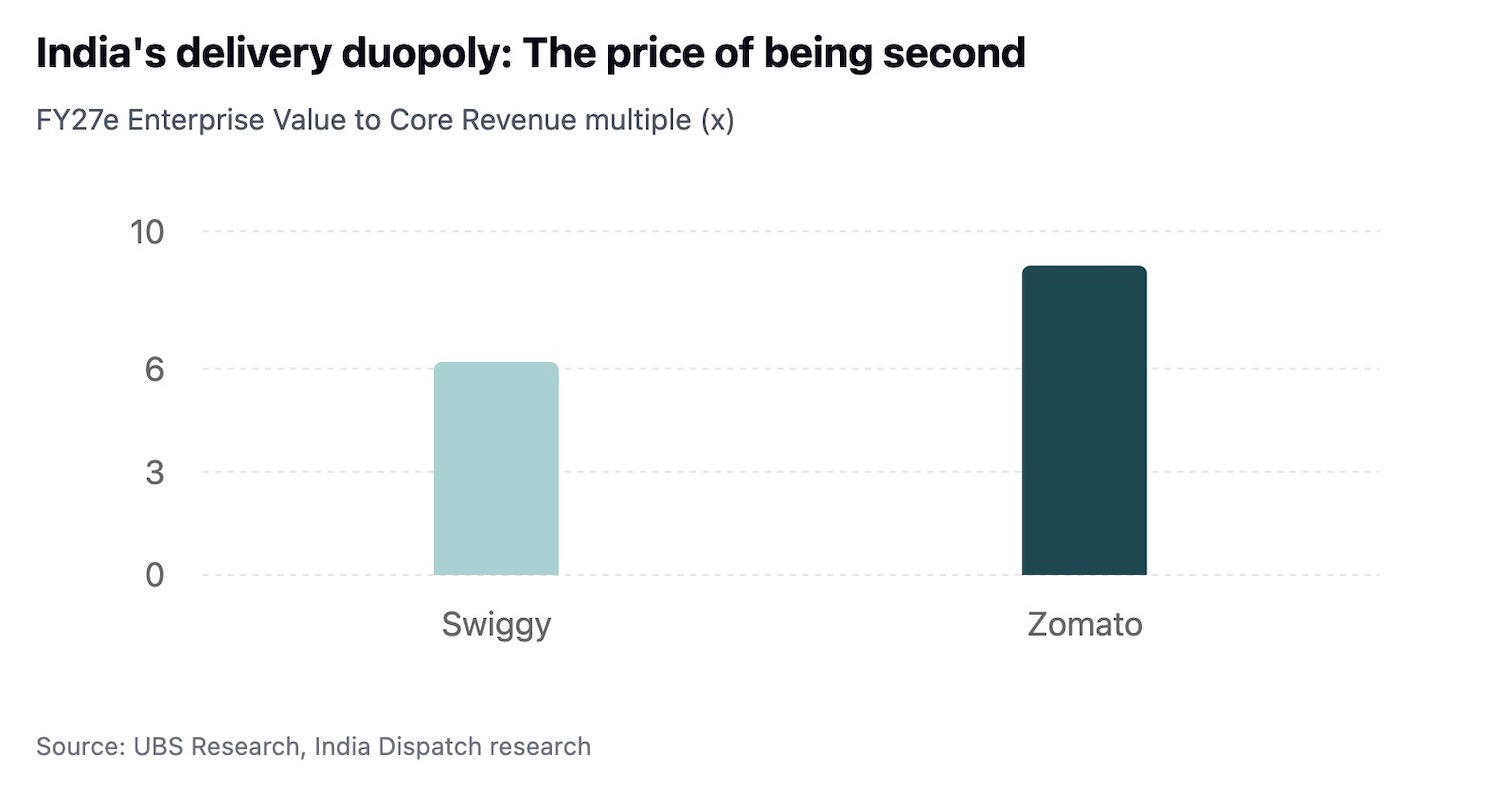

UBS has initiated coverage of Swiggy with what appears to be a rather intriguing observation. The bank’s analysts note that at current prices, Swiggy trades at an FY27 enterprise value to core revenue of 6.2x versus Zomato’s 9x.

The discount looks particularly peculiar given that UBS’s own receipt data shows Swiggy’s volume growth has largely matched Zomato’s since late 2023. Growth projections remain on similar trajectories for both the firms (Swiggy at 21% CAGR for FY24-27 versus Zomato’s 23%), both are burning cash in quick commerce, and both dominate India’s food delivery market.

To be sure, Swiggy’s margins lag Zomato’s by 12-24 months. But a 40% valuation gap?

What’s particularly striking is that even UBS’s bullish Rs515 price target would still leave Swiggy trading at a 20-25% discount to its rival.

In India’s winner-take-most digital economy, being first appears to be everything – even when the second player is virtually indistinguishable from the first.

Follow India Dispatch on WhatsApp.