Blinkit And You'll Miss the 75% Valuation Gap

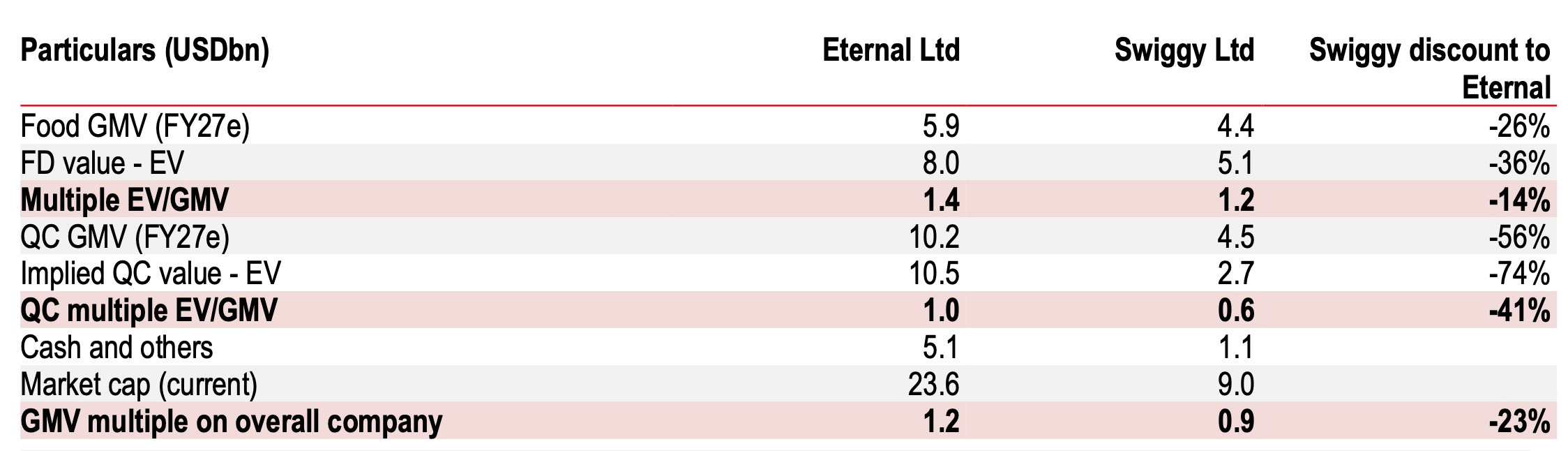

India’s quick‑commerce market is wrestling with an awkward valuation spread: HSBC values Eternal’s Blinkit at about $10.5 billion, while Swiggy’s Instamart is given a price tag of just $2.7 billion, a difference that means the market assigns almost four dollars of equity to Blinkit for every dollar it assigns to Instamart.

Although Blinkit’s present gross‑merchandise value is only about twice the size of Instamart’s, investors are capitalising those revenues at a substantially richer rate, translating into roughly two dollars of market cap per GMV dollar for Blinkit versus roughly one for Instamart.

HSBC’s model justifies the contrast by attaching a multiple of one times projected FY 27 gross order value to Blinkit while granting just 0.6 times to Instamart, even though both companies operate comparable dark‑store networks, deploy near‑identical fulfilment mechanics and confront the same emerging threats from Zepto and Flipkart Minutes.

Consistent profitability remains elusive on both sides of the duopoly: many analysts forecast that quick‑commerce losses will increase through the next few quarters and that the core food‑delivery businesses — which still generate most revenue — will expand only in the low‑to‑mid‑teen range, driven primarily by higher order frequency among existing users rather than by customer acquisition.

Instamart’s relative discount matters because, at a group level, Swiggy is valued at 0.9 times projected GMV versus Eternal’s 1.2 times, leaving Swiggy facing higher implicit capital costs just as cash burn across the sector accelerates.

Sector‑wide expansion plans add another complication: by late 2026 the industry is expected to operate more than 5,000 dark stores handling between $35 billion and $40 billion of annual orders. If Blinkit fails to convert its early scale advantage into meaningfully better unit economics, investors may start to question why twice the GMV warrants four times the valuation; until then, the 75% premium remains one of the more puzzling misalignments in India’s new-age internet market.

The current mismatch is hardly new: Swiggy’s shares even debuted at a 35‑40% discount to Zomato on an FY 27 EV‑to‑core‑revenue basis. UBS at the time argued that Swiggy’s 12‑to‑24‑month margin lag hardly justified a gap that wide.