In Defense of India's IT Industry

The cost of electricity does not run an enterprise.

A post written as a fictional memo from June 2028 by short-seller Citrini wiped roughly $10 billion off Indian IT stocks in a single session on February 24. The Nifty IT index fell as much as 5.3% that day, its worst drop since August 2023, hitting a 30-month low. TCS, Infosys and Wipro each fell 3-4%. The Nifty IT gauge is down roughly 21% in February, its worst month since 2003, shedding more than $68 billion in market value across the index’s ten constituents.

The report has been picked over enough by now, but I want to dwell on its India thesis for a moment. Indian IT’s export model was built on the cost arbitrage of Indian developers relative to their American counterparts, the report says, and the marginal cost of an AI coding agent has collapsed to the cost of electricity, so that value proposition is dead.

In this scenario, TCS, Infosys and Wipro see accelerating contract cancellations through 2027, procurement teams demand 30% renewal discounts, the rupee falls 18% against the dollar in four months, and the IMF begins preliminary discussions with New Delhi by the first quarter of 2028.

It’s a gut-wrenching scenario, but the argument is built on a model of the Indian IT industry that is roughly 15 years out of date.

India’s software and IT-enabled exports were roughly $205 billion in FY25, per the RBI’s annual survey of software export companies. The claim that this entire edifice was built on “one value proposition,” cheap developers, is a great misunderstanding of what these companies actually do for a living.

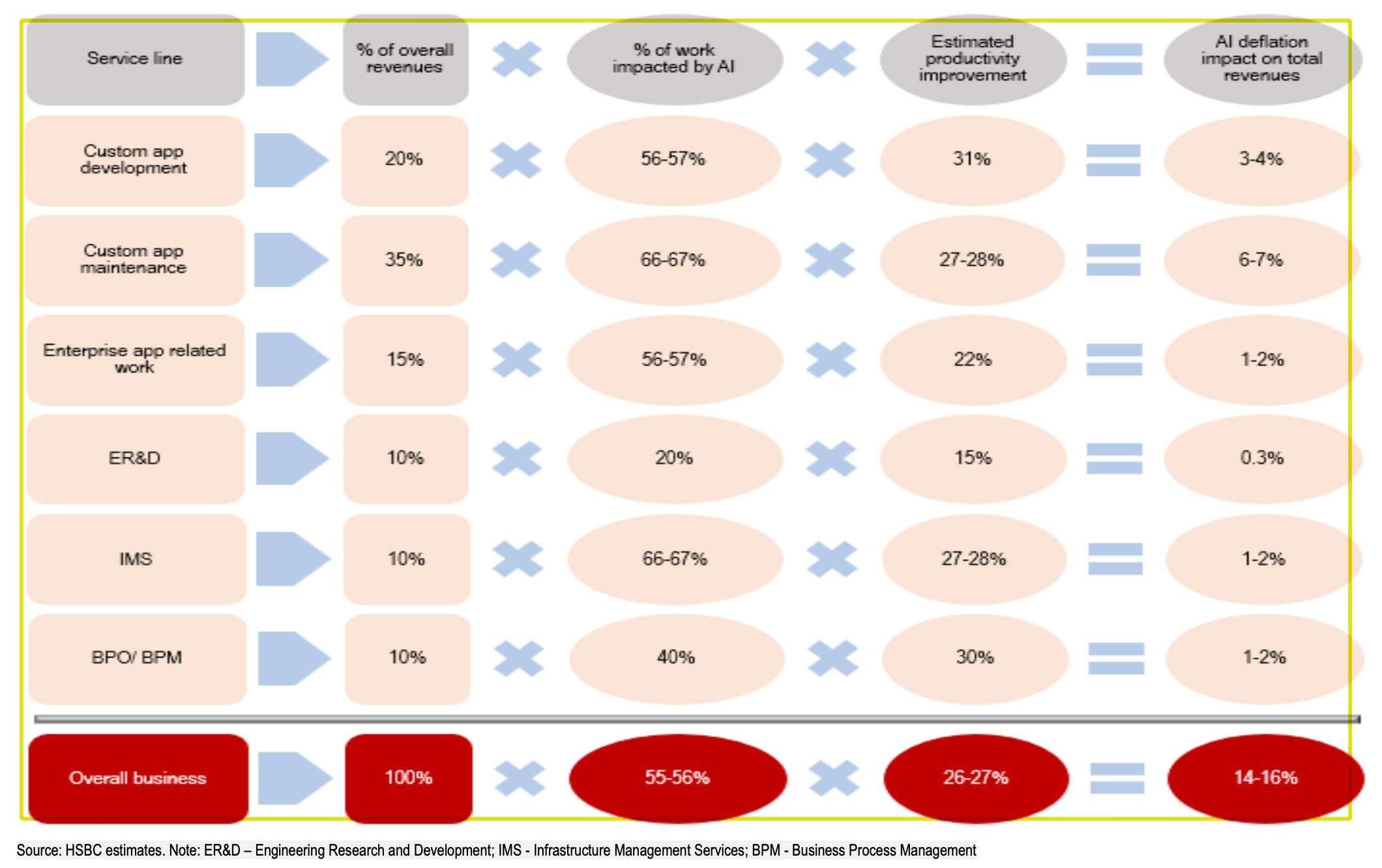

The technology stacks of the world’s largest enterprises are sprawling and non-monolithic, they take years to adapt to each new wave, and the work Indian IT companies do is overwhelmingly not greenfield coding. Custom application maintenance alone accounts for roughly 35% of a typical Indian IT company’s revenue, per HSBC’s service-line framework: incident management, service requests, change requests and problem resolution across architectures where SAP, Salesforce, Snowflake, Databricks, Guidewire and ServiceNow coexist in configurations unique to each client.

At an event this week, Anthropic shared a point that directly undercuts the “AI coding agent collapses the model overnight” narrative: the displacement risks that the firm itself highlighted are highest for job profiles involving data entry and project and technical documentation, not programming. There was no mention of the mean increase in coding productivity at the event, but the high end was pegged at 90%, mostly in recently established companies rather than those with long tenures and legacy codebases.

The gap between what AI can do to a two-year-old startup’s codebase and what it can do inside the accumulated infrastructure of a Fortune 500 enterprise is not a minor implementation detail.

These enterprise platforms require deterministic outputs, exact, repeatable, compliant, and AI is probabilistic, meaning its output can change every time the same question is asked. That mismatch is the core reason AI cannot wholesale replace the systems of record that form the backbone of enterprise IT. Enterprises will make AI behave more deterministically through context engineering, testing and governance, and Cognizant CEO Ravi Kumar flagged context engineering in his most recent earnings call as the key to making AI outcomes deterministic over probabilistic. Building and maintaining those guardrails is system integrator work, and not something a standalone coding agent handles at the cost of electricity.

AI does have a deflationary impact on the sector and it is not trivial. HSBC, in a note this week, raised its estimate of gross AI-led revenue deflation for Indian IT from 8-10% to 14-16%, broken down across 13 revenue sub-segments. Enterprise readiness is significantly lagging AI progress, HSBC also noted, echoing Infosys’s recent investor day, meaning the deflationary impact will likely take multiple years to fully materialise rather than arriving as a sudden cliff.

CLSA separately estimated overall effort reduction at 10-20% depending on service line exposure, application development and maintenance and BPO seeing the most deflation, cloud migration and consulting the least. A granular revenue headwind measured in percentage points, however, is a fundamentally different thing from an industry in freefall where the IMF shows up at the door.

These deflation numbers do not exist in a vacuum. Anthropic’s internal research finds that about 27% of AI-assisted work consists of tasks that would not have been done otherwise: scaling projects, building tools like interactive dashboards, exploratory work that would not be cost-effective manually. IDC projects GenAI to be net positive for IT services spend growth in 2026.

Bank of America argues the opportunity side is materially larger than the threat. About 62% of the value that AI generates for enterprises is expected to come from core business functions like operations, sales and marketing, and R&D, where IT services companies have an entirely new addressable market. IT as a support function accounts for only about 7% of total AI value generation, and that is the smaller bucket where deflation is concentrated.

Cognizant, at its recent investor day, put the current labour spend pools in core business processes, including R&D, sales and marketing, HR and customer service, at multiples of the IT services labour pool across every segment. The opportunity for providers of AI agents to help enterprises modernise those core processes is, on a spend-pool basis, significantly larger than the revenue at risk from coding automation.

The enterprises themselves are moving in this direction. Citizens Financial announced a multi-year initiative called “Reimagine” broken into 50 work streams, half of which are tech and AI-enabled. Bank of America has mapped all of its work into 3,700 processes and 55,000 individual activities as a prerequisite to deploying AI and expects technology spending to increase 5-7% in 2026 to more than $13 billion total, with over $4 billion in new initiatives. Goldman Sachs has identified six discrete work streams and assembled teams to underwrite all activities for efficiency opportunities.

These public announcements aren’t painting the picture of IT services contracts getting cut. They are evidence of the need for technology partners to deploy firm-wide transformation at a scale no AI coding agent can execute autonomously.

Anthropic itself has been building an extensive partnership network with system integrators to take its solutions to enterprise clients, and it’s not a strange — enterprise customers account for roughly 80% of Anthropic’s business and about 40% of OpenAI’s, which is why both are investing in SI partner ecosystems rather than going direct.

Accenture today struck a multi-year deal with Mistral AI to use the startup’s models to assist its own clients in leveraging AI, following a different partnership Accenture struck in December to train 30,000 professionals across financial services, life sciences and the public sector. Cognizant rolled out Claude to 350,000 employees in November. Deloitte rolled it out to 470,000 employees and began training 15,000 professionals in October. IBM announced a strategic partnership in October to infuse Claude into its software portfolio.

At the Anthropic event, the company described Claude Cowork making strong progress across data, legal, finance and banking, and emphasised that implementation is happening in partnership with firms like Accenture, Infosys, BCG and Deloitte to create offerings tailored to enterprise environments. Anthropic expects agentic architectures to evolve from single-agent workflows to multi-agent systems where an orchestrator coordinates specialised agents working in parallel across dedicated contexts, the kind of complexity that system integrators exist to manage.

The doomsday narrative on the Indian IT industry isn’t new. The claim that ERP would kill the application development and maintenance business turned out backwards, as SAP and Oracle ERP implementations became multi-year, multi-million-dollar projects. The claim that the shift to cloud and SaaS would cause significant volume shrinkage for IT services has played out, and software revenues including SaaS have grown at 3-4x the rate of IT services spend without destroying the sector. The claim that social, mobility, analytics and cloud selling required a heavy onsite presence that Indian IT did not possess also proved wrong, as cloud and data analytics are currently the fastest-growing service lines for Indian IT firms.

In the last major technology cycle, the shift to cloud, average organic constant-currency revenue growth for the top five Indian IT companies bottomed around FY16-FY18, re-accelerated from FY19, and the sector found itself re-rated. The narrative has always changed when earnings growth turned around.

Citrini’s broader macro argument is that IT services exports are the single largest contributor to India’s services trade surplus and finance its persistent goods trade deficit, so if AI destroys that revenue base, the surplus evaporates, the rupee crashes 18%, and the IMF shows up.

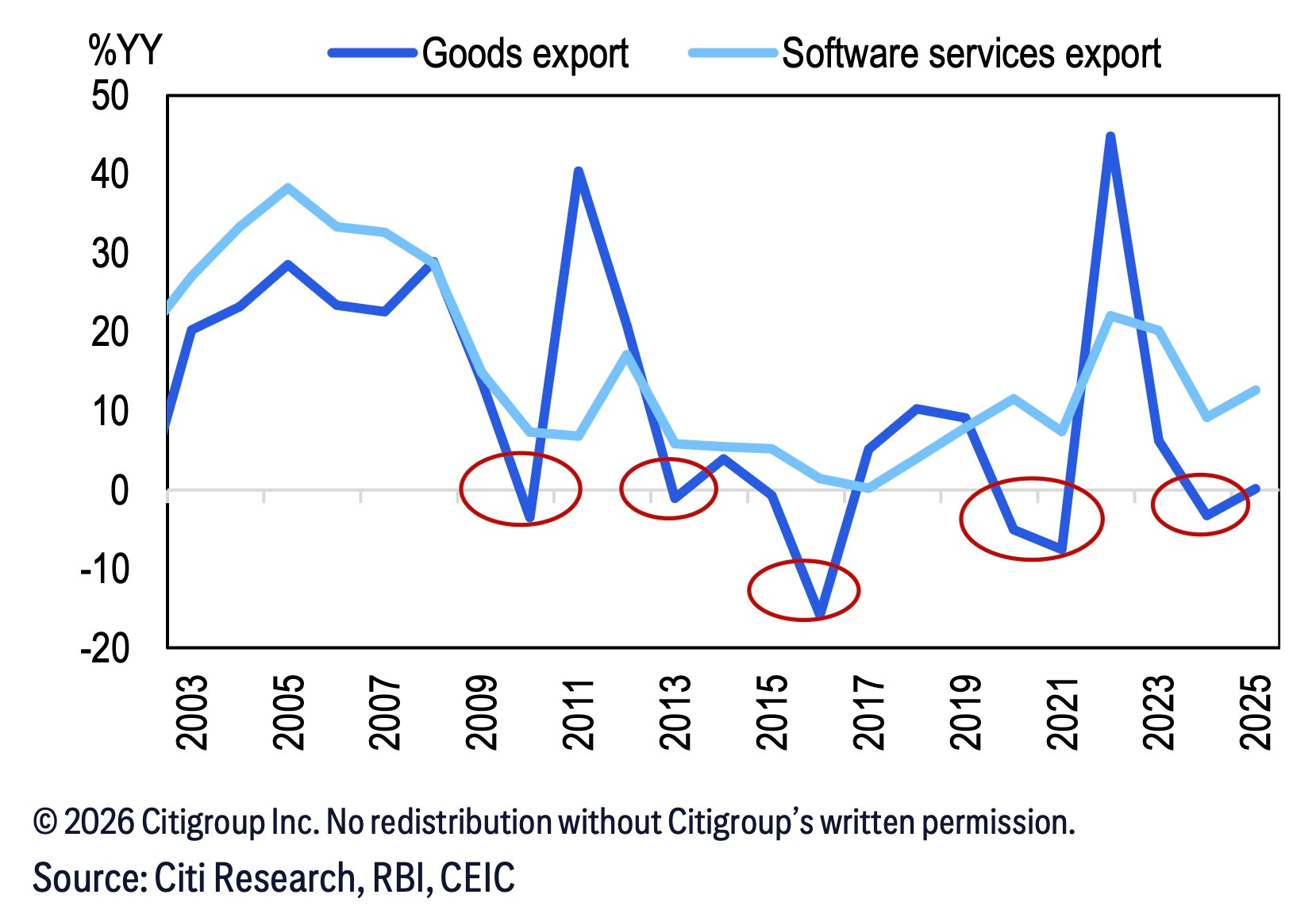

Citi’s economics team, analysing RBI data, offers a detailed counter. The 10-year CAGR for software services exports is 9.5%, against 3.4% for goods exports, and software services exports have never experienced a year-on-year decline in 24 years, not through the dot-com bust, the global financial crisis, or Covid.

Management and consultancy services exports, which include GCCs, have grown even faster at a 26.3% 10-year CAGR. The share of management and consultancy services in total services trade surplus has gone from about 13% pre-Covid to about 37% in FY25. Even in the most recent data, October 2025 through January 2026, after AI anxiety was already widespread, total services exports continued growing at roughly 12% year-on-year.

Citi does expect India to post a balance of payments deficit in both FY25 and FY26, the first consecutive deficits since at least 1991, driven by persistently low net FDI flows and a widening goods trade deficit. That is a real vulnerability and worth taking seriously on its own terms, but Citi’s analysis maps out exactly how bad the software export picture would have to get for the Citrini scenario to materialise, and the numbers do not support it.

In their base case of roughly 8% growth in software exports for FY27, the BoP returns to surplus at about $20 billion. Even if growth halves to 6%, the surplus holds at $15-17 billion. A scenario of flat software exports, zero growth, something that has never happened in 24 years, would reduce the surplus to $5-8 billion but still not tip India into deficit.

The Citrini scenario of a 5% year-on-year decline, accelerating cancellations and an 18% rupee depreciation requires something that has never occurred in the history of Indian software exports, sustained at a pace that outstrips every historical precedent including the worst global recessions of the past quarter century. It also requires ignoring that India is sitting on record foreign exchange reserves of $725.7 billion, enough to cover nearly 12 months of goods imports and about 96% of external debt, a buffer of a fundamentally different order from the early-1990s crisis that actually did bring the IMF to Delhi.

The on-site service share in total software exports has fallen to 9% in FY25 from 20% in FY16, meaning the sector’s immigration dependence is significantly lower than a decade ago. Geographical diversification is improving as the U.S. and Canada share has declined from 64% in FY13 to about 54%, replaced by Europe and Asia. The rising share of private limited companies in software exports, from about 35% in FY13 to about 60% in FY25, may partly explain the gap between listed company revenue growth and the resilience of aggregate software exports in RBI data, suggesting GCCs and unlisted entities are capturing a growing share of the export pie.

There is also an emerging structural opportunity that the Citrini narrative entirely ignores. HFS Research projects a category it calls Services-as-Software to grow from essentially zero today to $1.5 trillion, eating into share from both traditional software and traditional IT services. In this model, AI-driven autonomous delivery replaces seat-based SaaS pricing and time-and-material services billing, and pricing shifts to outcome-based and consumption-driven models. Salesforce has already moved from seat-based to consumption-based pricing, Accenture and Globant have made early moves, and more than 60% of enterprises plan to replace at least some of their professional services with AI-driven solutions by 2030, per an HFS survey of 1,005 major global enterprises. IT service companies proactive about building their own AI agents, and willing to cannibalise legacy revenues, can gain share from software companies rather than just lose it.

CLSA adds that GCC headwinds could turn into a tailwind as bloated GCC cost structures and the mainstreaming of AI push work back toward outsourcing, and that enterprises increasingly prefer to “build” over “buy” for AI-driven differentiation, increasing integration and customisation work for services firms rather than reducing it.

NSE IT now trades at roughly a 2% discount to the Nifty, against a 10-year average premium of about 15% and a 5-year average premium of about 29%. Indian IT has de-rated to approximately 17x FY27 estimated earnings. The sector’s problems are real: low- to mid-single-digit organic constant-currency revenue growth for large caps over the past three years, GCC competition for talent, IT services being crowded out in overall tech budgets. But a scenario that imagines IMF discussions with New Delhi because AI coding agents run at the cost of electricity is not a description of those problems.

The AI agents market is projected to reach $52 billion by 2030, growing at a 45% CAGR, per BCG. GenAI services software is growing at a 57% CAGR over 2025-29, per IDC. GenAI revenues already account for roughly 5-10% of total revenues for Indian IT companies and are growing fast: Accenture’s GenAI bookings reached $2.2 billion in the first quarter of FY26, or 10.5% of its overall order book, up from 0.4% in FY23, and TCS reported annualised AI services revenue of $1.8 billion, or 6% of overall revenue. CY26 organic growth guidance by Cognizant, Capgemini and EPAM is all coming in better than CY25, and multiple brokerages expect growth to exceed consensus in at least FY27 on cyclical tailwinds and a strong U.S. corporate earnings season.

In short: 24 years of software export data that has never posted a decline, $200 billion in annual revenue, partnerships with the very AI labs whose products are supposed to be the instrument of the sector’s destruction, possibly a new $1.5 trillion market category emerging at the intersection of services and software, and the largest U.S. corporates in the middle of mapping their entire workforces into process architectures that require technology partners to modernise. I think India’s IT is going to be fine.