India's Insurance Commission Problem

The regulator wants to cut what distributors earn, but distributors are the only reason protection gets sold at all.

When someone in India buys an insurance policy, the company that sells it typically doesn’t find the customer on its own. An agent, a broker, or an online platform like Policybazaar provides that service — and the insurer pays them a commission for it, a cut of the premium that can run to 30-40% in the first year. India’s insurance regulator, IRDAI, is now preparing to cap or restructure those payouts and draft regulations are expected within weeks.

IRDAI hasn’t announced anything yet, but recent language in the Insurance Act has revived a power the regulator has always technically had — the authority to dictate how much intermediaries can earn. The regulator ran product-level caps until a few years ago, setting specific limits on what agents and brokers could be paid on each type of policy. It then relaxed the regime, capping overall expenses rather than individual commissions, which gave insurers more flexibility in how they distributed their spending. The new statutory language means the harder power is live again, and people close to the industry describe a “new urgency” from the government around getting more Indians insured.

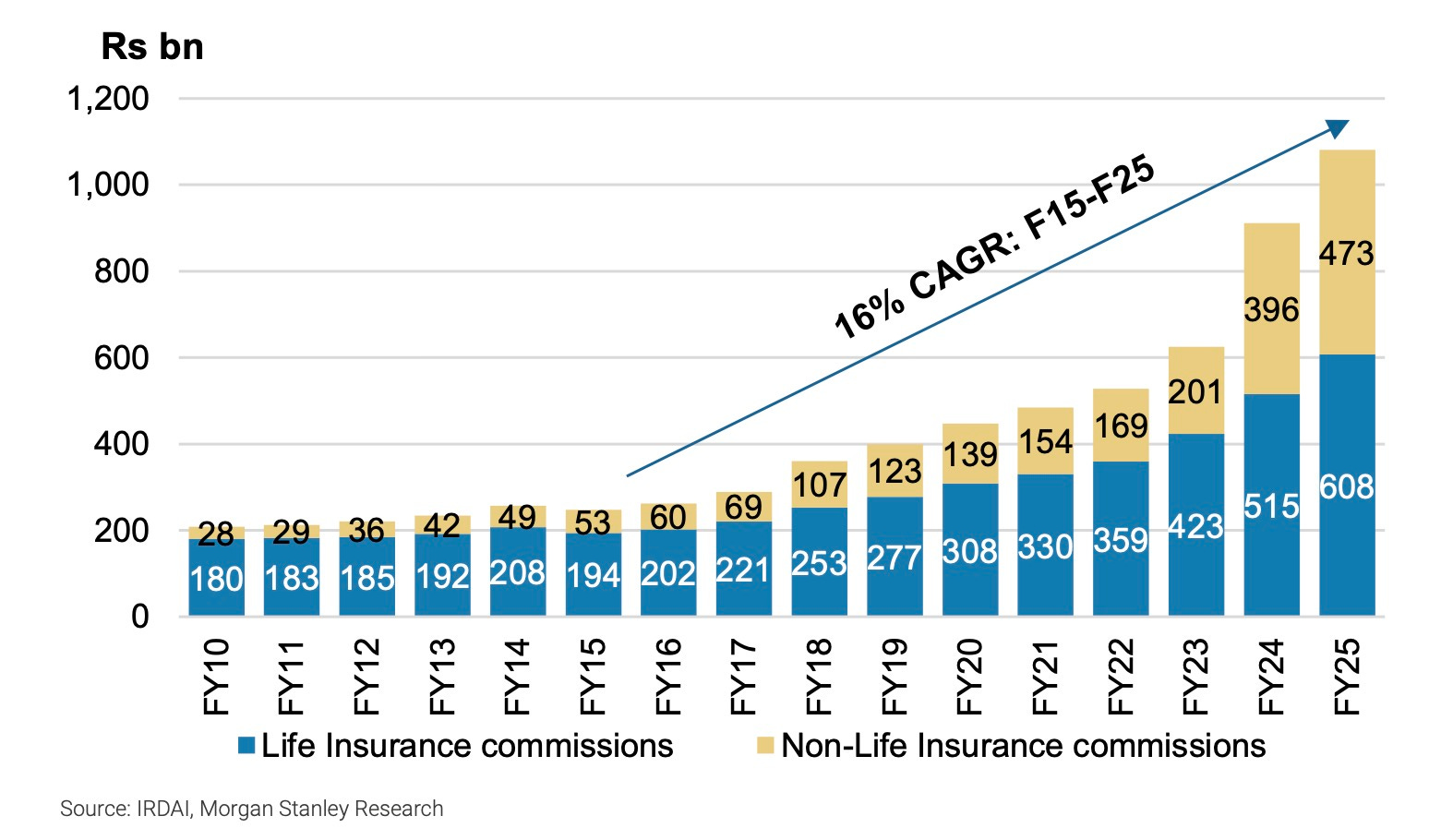

Insurers across the industry paid out $11.7 billion in commissions in the financial year that ended last March, a figure that has been growing at a 16% compound annual rate over the past decade, and private life insurer commissions alone compounded at 25%. In India, commissions are high and hence premiums are high, so the policymakers want to squeeze one so the other falls.

A cap would compress what intermediaries earn, but it would also reshape who holds bargaining power between the insurer and the distributor. In India, where finding and convincing customers to buy insurance is genuinely difficult, the distributor has historically had the upper hand.

Most of what the Indian insurance industry sells as life insurance is really a savings product with an insurance wrapper — a way for households to park money, earn returns and get a tax break while carrying some sort of death cover (however thin). Term life, where you pay a small premium and your family gets a large payout if you die, and standalone health insurance that covers hospital bills together account for only about 6-8% of the volume mix, and the rest is credit life and group insurance.

Tens of millions of Indian families have no meaningful financial cushion against death, disability or serious illness. If policymakers want “more protection, not more savings wrappers,” the cost of getting those products to people is the obvious target.

But protection in India isn’t bought the way it is in wealthier countries where people go looking for coverage. It’s sold through agents and call centres where a human being walks a reluctant and skeptical customer through a product they’d never seek out on their own, explains the terms and handles the paperwork. A commission squeeze works in countries where insurance is a pull product.

If protection is sold, not bought, the commission debate stops being about cutting fat. The government may be about to defund the only distribution engine that can push protection into Indian households.

For the largest online insurance broker, call-centre operations — the teams that phone potential customers, explain policies and close sales — run to roughly 40% of core revenue. Performance marketing, the digital advertising that generates leads for those call centres, adds another 15% — and those are direct costs, cuttable if commission compression stays shallow. Indirect costs — offline marketing, salaries outside the call centre, corporate overhead — run to another 20%, and industry executives insist these “may not be quickly reduced.”

One scenario analysis by Bernstein that is making the rounds models three levels of commission cuts. A shallow cut produces a 6% revenue hit and roughly 10% profit hit in the first year; a moderate cut takes those figures to 18% and 33%; and a deep cut reaches 30% and 61% — even assuming the broker immediately slashes costs in response. The market seems to have priced in deferral or shallow cuts, not deeper ones.

In 2018, SEBI, the securities market regulator, imposed a sweeping reduction in the fees that mutual fund companies could charge investors. That in turn compressed what mutual fund distributors — the agents and platforms that sold funds to retail customers — could earn. It was a consistent, pan-industry action that left distributors no choice but to absorb the reset and adjust. The insurance commission pool is arguably the largest fee income pool for distributors in Indian financial services, and a consistent, pan-industry action from IRDAI would put insurance distributors in the same position.

There’s also the question of when commissions get paid, not just how much. Intermediaries currently get a large share of their commission upfront, in the first year of the policy, even though the insurer’s economics depend on the customer continuing to pay premiums for years. A deferral regime would shrink the upfront payout and push more into renewal years, tying the intermediary’s income to whether the customer actually keeps the policy. The agent or broker would then have reason to sell the right product to the right person rather than whatever pays the highest first-year commission.

The intermediary’s costs, though — staff, call centres, marketing, the work of actually finding and onboarding the customer — all get spent at the point of sale. If the income from that sale gets pushed into future years, the intermediary may owe taxes on earnings it hasn’t yet received, because the commission is recognised as income even if the cash hasn’t arrived. If the cash inflows is pushed out, the pressure isn’t just on margins but on working capital — the day-to-day cash a business needs to keep operating.

Some scenarios being modelled say that if cuts go deep enough, the call-centre model of assisted selling stops working entirely. For the largest online broker, that model is described as “critical” to selling health and term life — the exact products policymakers say they want more Indians to own. The distribution channel that has been reaching consumers who would never have bought protection otherwise can come to a halt if the economics changes.

Agent productivity in the traditional agency channel — the individual agents who sell policies door to door or through personal networks — is also heavily skewed. Most of the business comes from a small percentage of productive agents who are likely to stay committed even with lower payouts. The long unproductive tail that could become more disengaged wasn’t generating much volume to begin with. The deeper vulnerability is the call-centre model, where costs are fixed and high, and where the economics of selling protection to people who don’t want it depends on upfront commissions covering upfront acquisition costs.

Some investors and other industry executives say insurers might eventually get nudged to build their own web and call-centre sales engines “alongside” the intermediary ecosystem — doing the selling themselves rather than outsourcing it to brokers and agents. A commission policy dressed up as consumer protection could end up pushing the industry to bring distribution back in-house. If the economics for intermediaries shrink and protection still has to be actively sold to people who don’t want it, the insurer might be the only one left who can afford to do the selling.

If insurers build out direct channels, bargaining power shifts their way; if intermediaries figure out how to sell efficiently even with restructured payouts, it shifts back. The balance ahead of the draft regulations appears tilted in favour of insurers — especially large, disciplined ones who stand to gain from lower distribution costs if implementation is strict.

One model floating around PB Fintech, the parent company of Policybazaar, goes in a different direction — toward profit-sharing with insurers, curated product shelves where only vetted policies are offered to customers, and delegated authority where the platform takes on underwriting and claims work that insurers normally do themselves. Other markets call this a “managing general agent” or MGA, an intermediary that does more than sell, helping design and run parts of the insurance operation, paid like a partner rather than a salesperson. (Non-banking financial companies, or NBFCs, grew into something similar in lending — origination-and-servicing machines that found borrowers, assessed their creditworthiness and managed loans, work that banks couldn’t or wouldn’t do themselves, especially in smaller cities and rural areas.)

If commission levels become politically sensitive and regulators want every rupee paid to intermediaries justified, the survivors will likely be the ones who can argue performance, not volume.

Absolutely love your work Manish but please title this - life insurance. Being from general insurance sector, it pains me to see how (Still) generic the use of insurance as a term is.

Also, govt came for gen insurance commissions as well and it had some interesting effects long ago. Thanks!