India's Missing Magnet

India's equity premium, IPO pipeline and China+1 pitch all depend on capital that has stopped arriving

TOKYO, Japan - India’s rupee has fallen about 14% against the dollar over the past year. The dollar itself has been essentially flat against other major currencies over the same period, making the weakness idiosyncratically Indian. The current account, contrary to some chatter on social media, is narrow at 0.8% of GDP, the lowest on record. The real squeeze is on the capital account, where foreign investment has completely dried up.

That capital has underwritten India’s equity premium over emerging-market peers, the heavy IPO pipeline and the country’s positioning as the natural alternative to China. All three depend on it continuing to arrive.

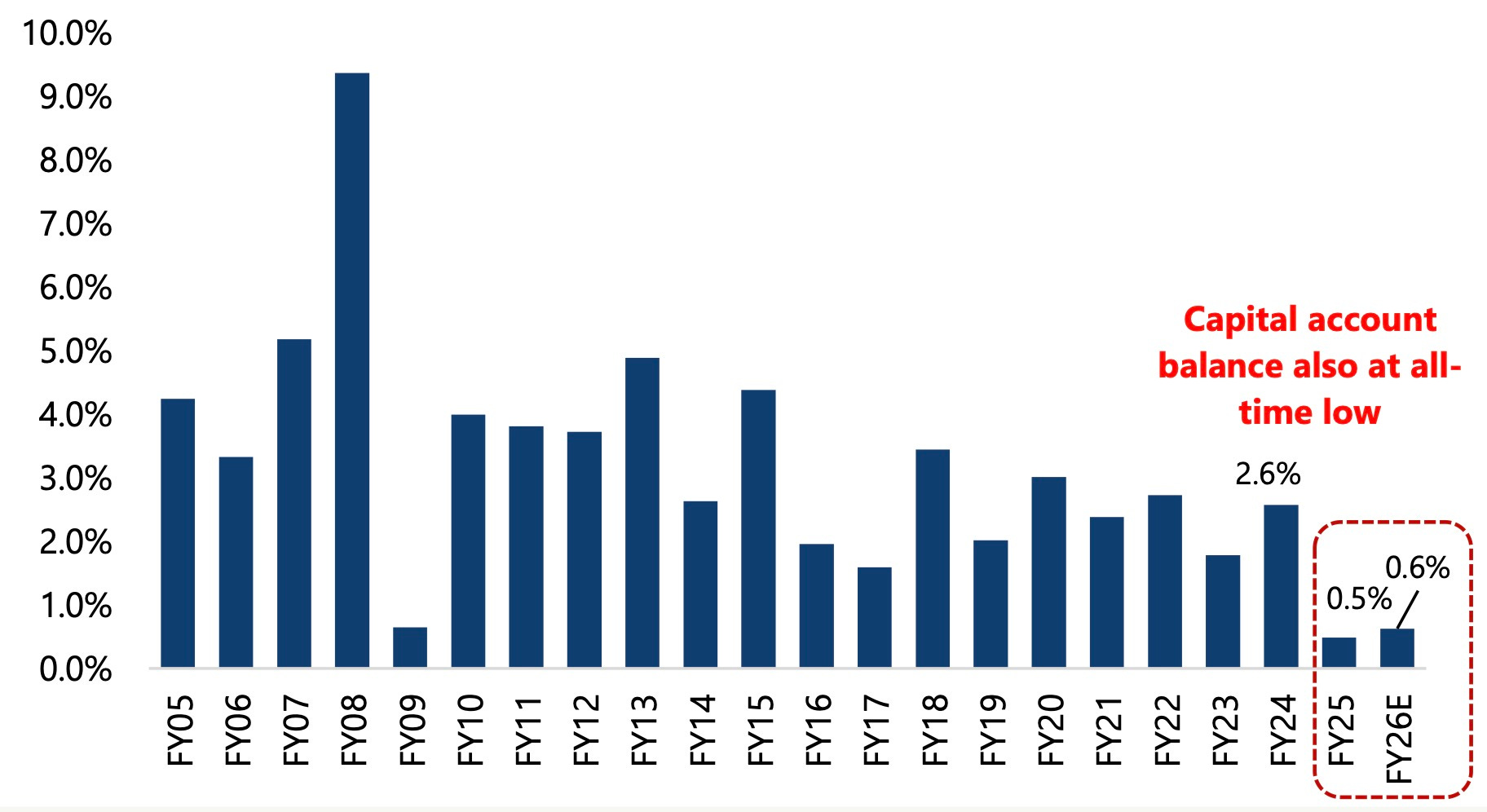

Capital flows that averaged 2.6% of GDP between 2015 and 2019 slowed to 1.4% in calendar 2024 and dried up in calendar 2025. Per RBI data, the FY25-26 capital-account surplus was 0.5% of GDP, also the lowest ever.

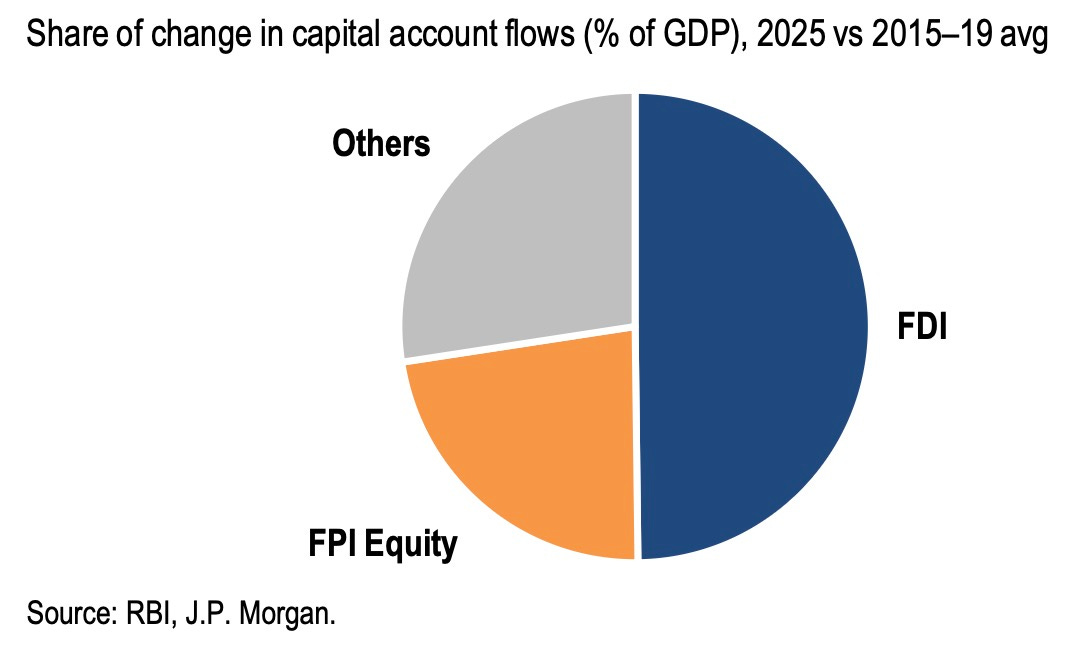

Net foreign direct investment, the money foreigners put into Indian factories and businesses minus what they take out, ran at 1.5% of GDP before the pandemic and now sits at 0.1%. India received about $5 billion of net FDI cumulatively over the past two financial years, against a single-year peak of $44 billion in FY21.

All three components of net FDI have moved against India. Gross inflows have softened, profit repatriation by foreign investors has risen from $45 billion in FY24 to about $54 billion projected in FY26 and outbound investment by Indian residents has climbed from $17 billion to $35 billion over the same stretch.

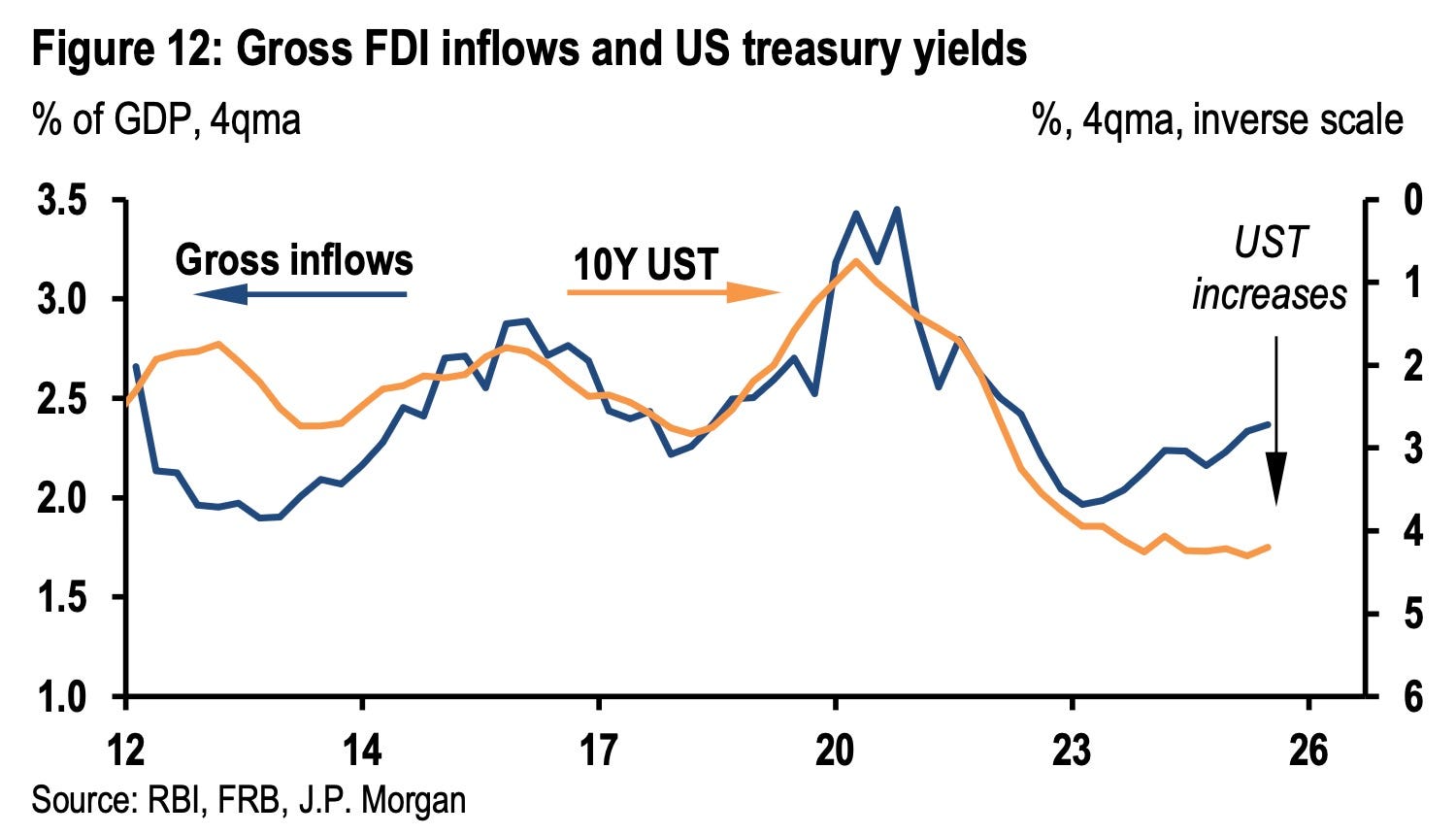

India has not had a contemporary draw for foreign capital since 2010. Between 2005 and 2010 a private investment boom drew it in. Since then its net FDI has tracked US 10-year Treasury yields, arriving when American rates fall and retreating when they rise. Foreign capital today flows to emerging markets that offer that draw, like North Asia for AI and semiconductors, Latin America for commodities or Vietnam for the manufacturing that moved out of China during the trade war.

India, in comparison, has a large consumer market, strong banks and other companies, but also a high valuation and increasingly no draw of its own.

AI is the clear solution, but India has little listed exposure to chips, computing infrastructure or foundation models that drive global AI. The opportunity in India, Bernstein argues, is in the physical build-out, the data centres, electrical equipment, cooling, cables and civil construction, where less than half of a possible $300-450 billion investment would go to Indian suppliers. The recurring $16 billion to $20 billion a year that Indian consumers and businesses will spend on AI services flows out to the global platforms that collect the fees.

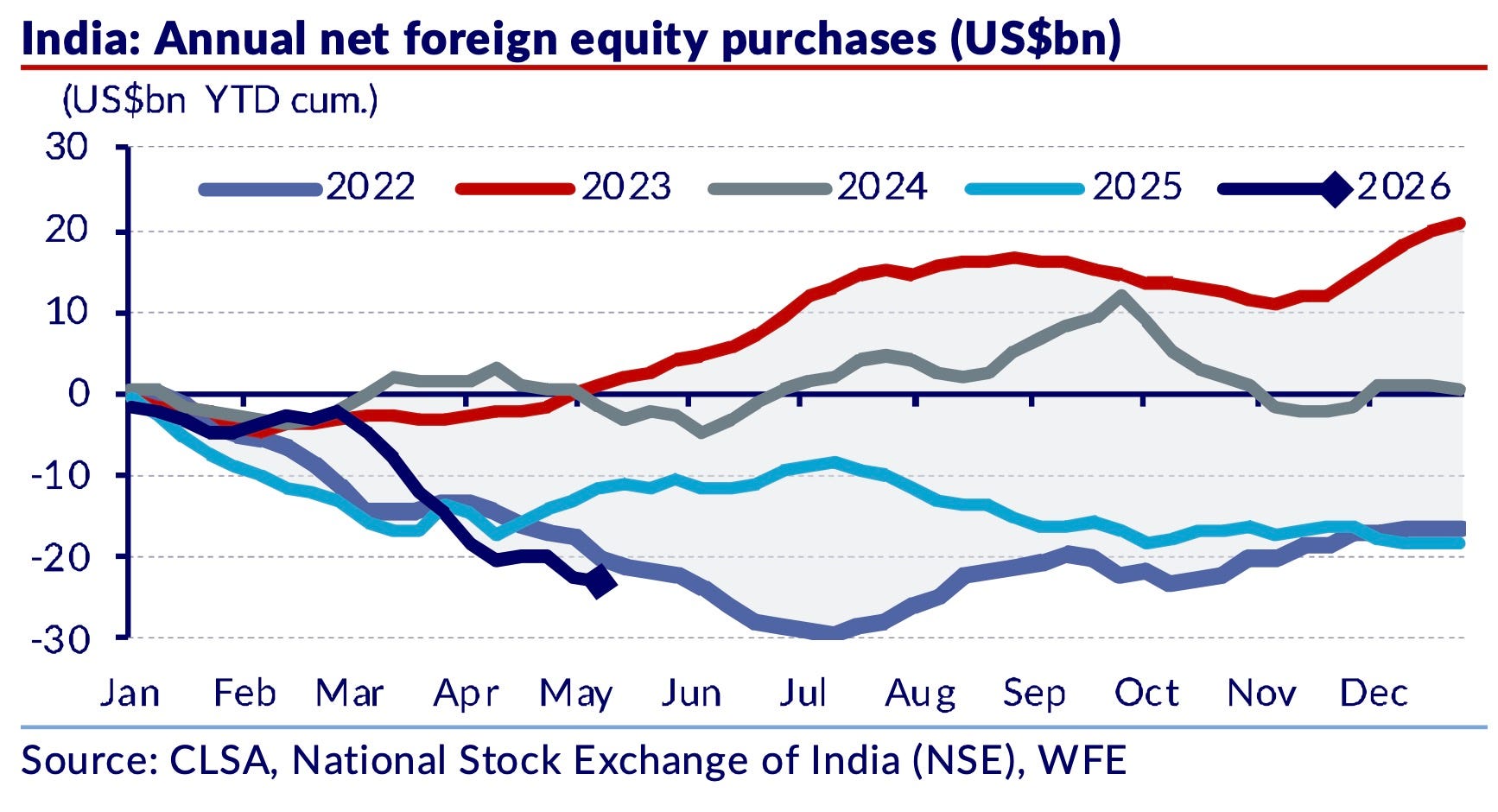

Foreign investors sold a cumulative $78 billion of Indian equities over the past two years, according to securities depositor NSDL. Foreign portfolio investors accounted for 47% of the selling, private-equity firms for 33% and foreign promoters, the founder-owners of Indian companies, for 20%. Net foreign portfolio selling in equities alone hit a record $21 billion in FY26 and has continued into FY27.

Per fund-flow data, India was the least-favoured emerging market in April, even after global risk appetite picked up. The Nifty index rose 7.5%, its best month since December 2023, and foreign institutional investors still sold $5.2 billion of Indian shares. Non-India active funds sold $2 billion that month, India-dedicated active funds $1.7 billion and passive funds $1.6 billion.

Indian mutual-fund inflows held up at $7.5 billion but were 23% lower than the previous month, according to an analysis of data from industry body AMF, and the share of monthly SIP subscriptions being cancelled exceeded fresh subscriptions for a second month running. This is the downside of SIPs, where the recurring monthly money from Indian retail investors and pension funds becomes the exit liquidity for foreign capital escaping an expensive market.

Investor meetings have found clients confident in continued domestic flows, Goldman Sachs said in a note this month, but they are not expecting foreign capital to return soon. The reasons given have been the weak rupee, less attractive returns relative to other emerging markets and shrinking passive money as India’s weight in global stock indices fades. A recent fourth-quarter snapshot of Indian equities had earnings growth running at about 9% year-on-year, consumption steady to improving and valuations near long-term averages.

Indian services exports grew 14% in FY26 to $217 billion, per RBI data, covering 65% of the goods trade deficit and keeping the current account narrow despite rising oil bills.

The trigger for the current squeeze is the conflict in West Asia and a sustained spike in crude prices. India imports 88% of its crude, according to Petroleum Planning and Analysis Cell of the Indian oil ministry, and Russian oil exemptions have just expired, sending refiners back to Middle East suppliers. If crude averages above $100 a barrel through end-2026, the current-account deficit could rise to about 2.5% of GDP, or close to $100 billion, JPMorgan cautions.

Per official data, the Middle East accounts for 17% of Indian exports and 38% of remittances from Indians working abroad, an exposure that runs well beyond oil. A weaker rupee absorbs some of the pressure but not all of it. If it falls too fast, foreign investors and Indian companies start hedging their existing exposure, which adds to the selling.

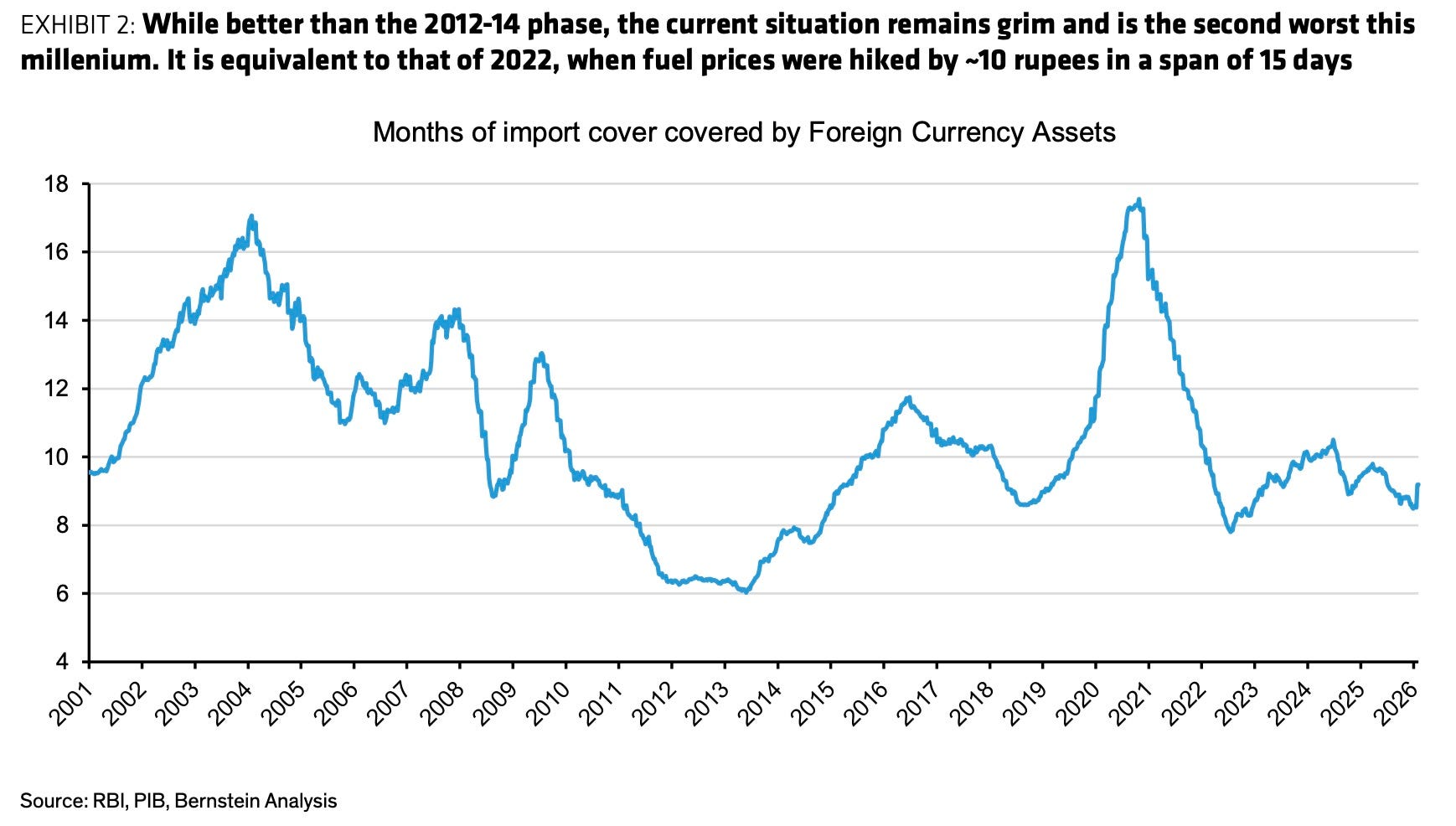

India’s foreign exchange reserves are down 4.3% since the West Asia conflict began, according to RBI data. The trailing 12-month import cover stands at 9.2 months against a long-term average of 10.7 months, the worst reserves position since the 2013 taper tantrum, when the U.S. Federal Reserve’s plans to wind down stimulus triggered a sharp emerging-market sell-off.

Reserves stood at $691 billion at end-March 2026 against $668 billion a year earlier, according to RBI’s official disclosures, and import cover was holding high. By mid-May the headline figure had fallen to $597 billion. After adjusting for $100 billion in forward dollar sales the central bank has yet to settle, that gives roughly 9 months of import cover, below average but still substantial.

The Reserve Bank of India had $78 billion in net short forward dollar positions as of February 2026, a 45% rise in six months. Of that, $28.5 billion comes due within 12 months and will draw down the headline reserves number when the contracts settle.

Prime Minister Modi has called for restraint on foreign spending and fuel use, in what analysts call exhortations on austerity and fuel conservation. The government has banned sugar exports, raised petrol and diesel prices by Rs3.9 a litre and pushed the gold and silver import duty to 15%, the highest level since 1991.

The current fuel-price cycle is at about 3.2%, against an average of around 11% per cycle over the past decade. The gold duty cannot easily be raised further, because Sovereign Gold Bonds from 2018-19 mature later this year and the government’s payout rises with the duty.

The 2014 playbook of attracting non-resident Indian deposits is harder this time because the gap between Indian and US interest rates is narrower. All the rate cuts expected this year may already have been priced out. If bad monsoons and fuel prices push inflation above the Reserve Bank’s tolerance band, inflation prints by July could push the conversation toward rate hikes instead.

The current moment is India’s fifth austerity cycle since liberalisation. There is stress on both the current and capital accounts, and the balance of payments is expected to stay negative for a third straight year. India in 2013 had double-digit inflation, negative real interest rates and a current-account deficit near 5% of GDP, and the Reserve Bank tightened sharply. Today inflation has averaged 2-3% for two years, and the expected pickup in private business investment has not arrived.

JPMorgan’s textbook playbook is expenditure switching first, where the rupee falls enough to make foreign goods more expensive and tourism abroad costlier so Indian buyers and travellers spend less of their money outside. Expenditure compression, in which the central bank or the government tightens credit and spending to slow the economy down and shrink imports, is the last resort.

The practical menu starts with squeezing outflows. The government can tighten Liberalised Remittance Scheme limits, raise customs duties on non-essential items and restrict certain imports outright. To pull capital in, it can lower taxes on foreign portfolio investment, sweeten terms for non-resident Indian deposits and ease external commercial borrowing rules for Indian firms.

Per RBI data, the rupee’s real effective exchange rate, an inflation-adjusted measure against a basket of trading-partner currencies, is at a 12-year low of 91, or roughly 9% undervaluation. The index has rebounded from this level in past episodes.

In the four past instances when the rupee fell more than 10% in 12 months, foreign portfolio inflows rebounded in three of them within the following 12 months. The exception was the 2008-09 global financial crisis.

At the end of the day, there are no easy answers. Foreign capital wants export categories that grow without subsidies, a real pickup in private capital spending and manufacturing FDI that arrives because foreign companies need India rather than because India has paid them to come. It also wants Indian technology businesses that own the intellectual property they sell rather than service someone else’s.