Why Indian Consumer Giants Don't Do Debt

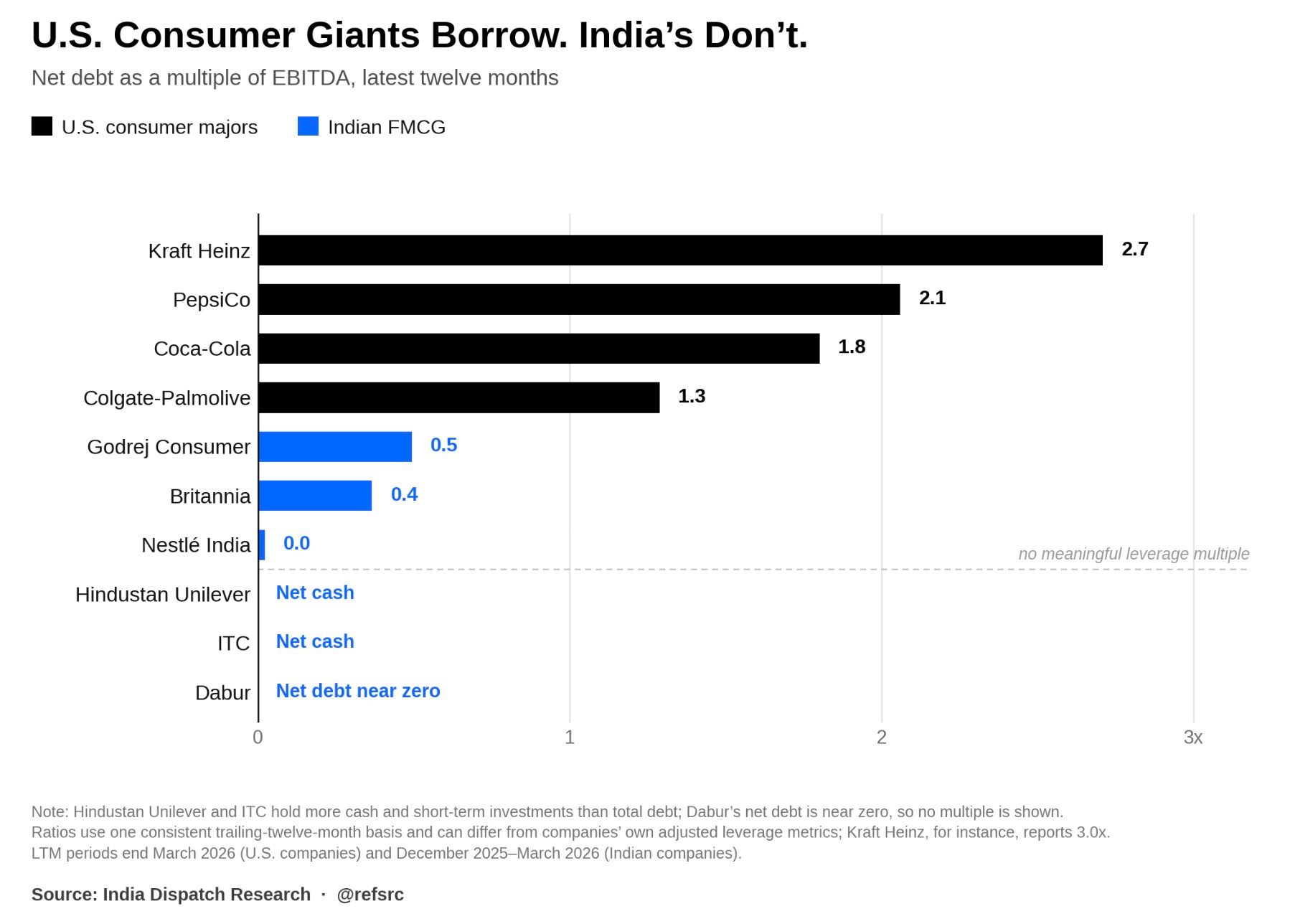

Hindustan Unilever ended FY26 holding $640 million more in cash and short-term investments than debt, while global consumer giants run two to three times levered.

FMCG companies – those that sell groceries, drinks and household essentials – earn the kind of cash flow that makes them suitable for carrying debt. Demand for staples tends to hold through most conditions, the products turn over quickly and because interest payments are deductible, borrowing shelters profit from tax. Modigliani and Miller put a number on that shelter in 1963: a firm carrying debt is worth more than an identical firm without it, by exactly the value of the tax its interest payments will save.

In developed markets, that is how the business gets financed. Unilever closed 2025 holding roughly $27 billion of net debt, twice its underlying EBITDA and Nestle ended the year at 2.85 times. Kraft Heinz carries $21.2 billion of debt at 3.0 times net leverage. This phenomenon has been going on for decades. KKR’s $25 billion purchase of RJR Nabisco in 1988, then the largest LBO, took a food-and-tobacco group private on borrowed money its own cash flows would have to repay.

Hindustan Unilever, which sells many of the same brands as its parent, closed the fiscal year ending March with cash and short-term investments exceeding its debt by roughly $640 million. Nestle India carries almost no borrowings, and ITC, the sector’s largest company by revenue, is for practical purposes debt-free.

A study published in Asia-Pacific Financial Markets charted this pattern on a broader footing — not the gap between India and the West, but which Indian firms borrow and which don’t. The researchers followed 77 FMCG companies listed on the BSE from 2012 to 2023 and asked which traits of a firm push its borrowing up or down: profitability, liquidity, tangible assets, tax rates, sales growth, age and size, each tested against short-term, long-term and total debt as a share of assets. In the fixed-effects model they settle on, nearly everything that matters pushes borrowing down. Larger firms hold less debt on every measure, while older firms, more liquid firms and firms richer in tangible assets hold less on the short-term and total measures, all of it statistically significant.

A firm paying a high effective tax rate has the most to gain from deducting interest. In this sample those firms hold less long-term and less total debt, significantly so in both cases, and the paper itself sets the result against the tax-shield benefit Modigliani and Miller proposed. Profitability points the same way on all three measures, though never significantly.

Sales growth was the exception. Faster-growing firms take on more long-term debt, which the authors attribute to expansion outrunning internal resources. The behavior matches the sequence Myers and Majluf described over four decades ago, in which a company funds itself from retained earnings first, turns to debt when those run short, and issues equity only when nothing else will do. The paper concludes its sample sits predominantly inside that pecking order, held there by imbalances in the information available to investors.

Within the sample, the explanation runs through information. A firm holding few tangible assets meets equity markets that mark its shares down, and reaches for debt as a consequence; a firm holding collateral, liquidity and scale escapes the discount and funds itself from inside. The largest companies may prefer the conservative position because alternative funding sits within easy reach, the paper suggests, and the oldest tend to live on retained earnings.

The study explains India against India, though. It cannot explain Unilever, which is larger, older and more liquid than anything in the sample and still runs at twice EBITDA. Part of the answer is ownership. Hindustan Unilever and Nestle India do not set their capital structure independently — they pay out most of their earnings as dividends and pay royalties to the parent, and the group borrows where debt is cheapest, which is not India. Unilever’s two times already consolidates its subsidiary’s cash. The cleaner test is the Indian-owned names: Dabur, Britannia and Godrej answer to promoter families in India, ITC has no controlling parent at all, and the most levered of the four runs net debt at about half its annual EBITDA.

Profitability is controlled for separately in the regressions, so the firms holding less debt at higher tax rates are not simply profitable self-funders in disguise; the simpler reading is that the shield is not worth chasing. A rupee of interest saves about 25 paise of tax under the concessional regime introduced in 2019, down from roughly 35 before it, while borrowing in India costs more than it does in the markets where the parents raise debt.

This doesn’t describes a sector that has sworn off borrowing altogether, though the study’s debt measure needs a caveat. The paper defines its ratios simply as short-term, long-term and total debt over assets, and the averages it reports — total debt at 52.8% of assets, 38.5% at the short end against 14.3% long-term — are far more than listed FMCG companies carry in actual borrowings. Numbers that size are consistent with a measure that counts operating liabilities, the unpaid suppliers and short-dated obligations that fund inventory in an industry the paper calls highly competitive, low on margins and dependent on substantial working capital.

At the very top of the sector, even that working-capital requirement belongs to someone else. Nestle India has collected from its customers in about four days while paying its suppliers in roughly 52, and Hindustan Unilever runs similarly, holding creditor days at 64 against receivable days of 16. Both figures date to 2020; on FY26 numbers Hindustan Unilever’s receivables run near 19 days of revenue against payables near 76, and both companies have operated on negative working capital for more than a decade. The distributors and suppliers finance the leaders’ operating cycle, removing their need for even short-term borrowing and pushing the financing burden down the chain.

Booth, Aivazian, Demirguc-Kunt and Maksimovic documented in 2001 that firms in developing countries rely less on long-term debt than developed-market peers, and a 2020 comparison across developed and developing markets finds overall debt ratios lower in the latter. Indian listed companies as a group have been shedding debt for years: the debt-to-equity ratio for listed non-finance companies fell to 0.5 in FY25, a record low on CMIE data covering more than 4,000 firms.