The House Always Wins

India's options exchange is the surest bet in a market where most punters lose. It is now selling shares.

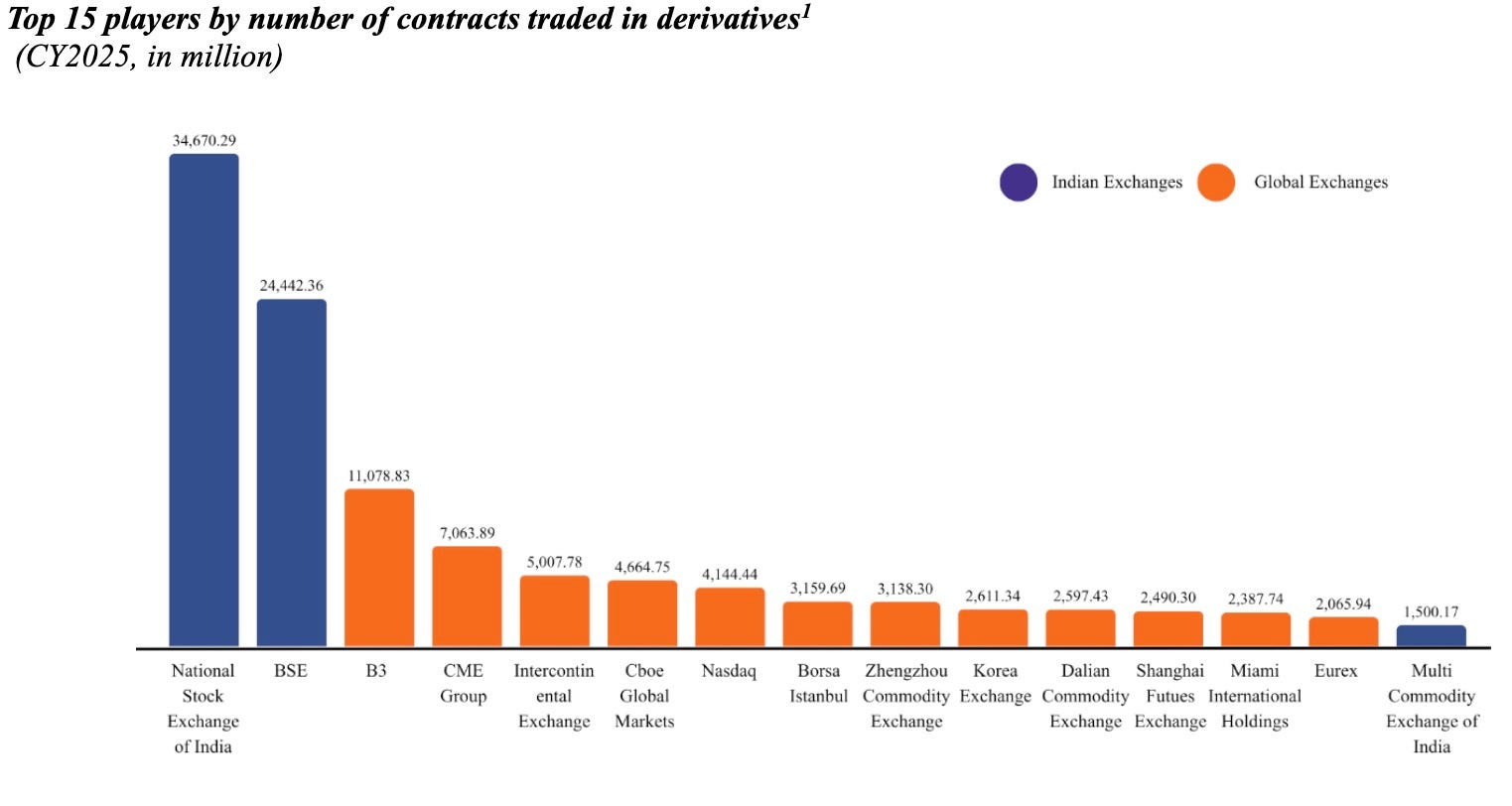

More derivatives contracts change hands on India’s National Stock Exchange than on any other bourse in the world — more than on the CME, Cboe, Nasdaq and the rest of America’s exchanges combined. India now accounts for more than four-fifths of all the equity options traded on earth, a share that was nearer a seventh a decade ago. Most are index options a fraction of the size of an American contract, bought a few dollars at a time. Nine in ten of the individuals who trade them lose money. The exchange powering this market is going public, after several delays.

Indians once bought shares through brokers who shouted prices across a hall in Bombay. NSE opened in 1994, put that market on a screen and broke the cartel that had run it for more than a century. It now carries almost every share and derivative traded in the country, counts 129 million Indians as registered investors and reaches more than 99% of the country’s postal codes.

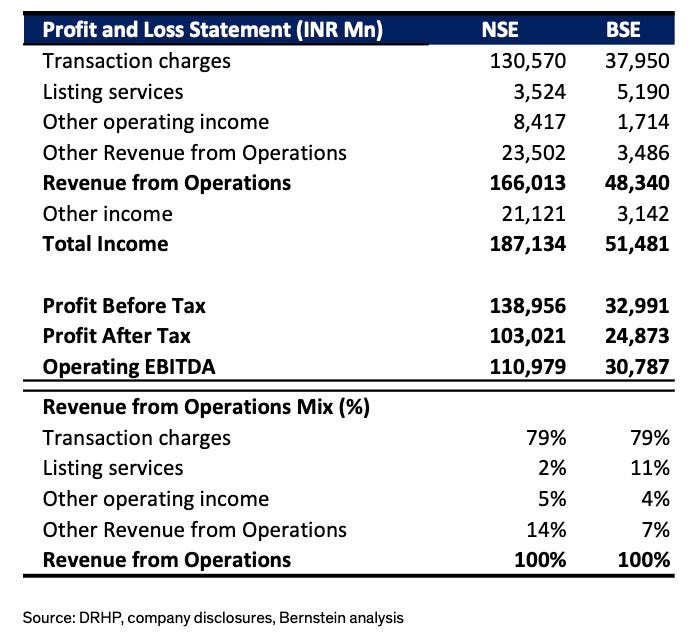

NSE is paid when Indians trade rather than when they own, win or lose, and the trade it leans on most is a short-dated, leveraged bet on the level of an index, the average one held for less than half an hour. Transaction charges supplied 79% of revenue last year, and equity options alone supplied 60%. A single S&P 500 option is about 37 times the size of a Nifty one, so the figure that ranks NSE first in the world counts tickets traded more than the risk they carry.

It is selling about 6% of itself to the public. The company itself will raise nothing, names no controlling owner, and will list the shares on BSE, the Bombay exchange it long ago overtook.

NSE made a net profit of $1.1 billion in the year to March 2026, on the highest operating margins of any big exchange in the world. A company this dominant rarely shrinks. In fiscal 2026 it did, as revenue slipped to $1.75 billion from $1.81 billion and profit fell further, from $1.29 billion. Its market share barely moved, so the cause lay elsewhere.

NSE set aside $147 million last year to settle the colocation case, the long-running matter in which SEBI, the market regulator, alleged that some brokers had been given faster access to the exchange’s systems than others. SEBI barred NSE from the securities market for six months in 2019 and ordered it to disgorge $66 million, a tribunal later overturned the order, the Supreme Court has yet to rule, and in March 2026 NSE offered $157 million to close the matter. Most of the year’s fall in profit is that single charge, and that NSE can list at all in 2026 follows from the same settlement.

As a piece of market infrastructure NSE says in its prospectus IPO filing that it must put regulation, compliance, risk management and investor grievances ahead of its own business, and keep a wall between the staff who police the market and those who sell access to it. Its public-interest directors are bound to place the market above the interests of shareholders. A buyer of the stock owns a claim on profits the firm is required to give up whenever the integrity of the market demands.

About 91% of individual derivatives traders ended the year to March 2025 in the red, by the regulator’s count, and their combined net loss came to around $11 billion, close to ten times NSE’s profit. More than 40% of them are under 30, and about three-quarters earn less than $6,000 a year.

Proprietary desks that make markets in NSE’s index options supply about half of their turnover, and foreign firms under a tenth, the rest coming from retail. Much of what the punters lose is won by the firms taking the other side. The regulator barred one of them in 2025, the American quant trader Jane Street, froze about $570 million of its profits and accused it of manipulating index levels to profit from its own positions.

SEBI has spent two years trying to cool the betting, cutting each exchange to one weekly index expiry, raising the minimum size of a contract, demanding option premiums upfront and tightening limits, while the government has raised the tax on options. The number of active traders has since dropped by about a fifth, and the volume of options by some three-quarters in five months, a fall large enough to drag global options trading down by roughly half. The prospectus’s own forecasts put the market’s growth at about 10% a year from here, against nearly 50% over the past decade.

The betting is fed by an industry of self-styled trading gurus. One who called himself the father of charts drew nearly 4.4 million YouTube followers and made about $1.8 million, the regulator said, from courses that promised returns of 200% to 300%, before it banned him and he resurfaced two years on. Another, barred in January, had taken about $63 million from clients for stock tips while his own trades lost money. The regulator pulled 162,000 posts and accounts from Instagram, Telegram and YouTube between April 2024 and May 2026, and built a tool named after a Hindu god’s spinning blade to find more of them across the country’s twenty-odd languages.

NSE’s contribution to the exchequer in fiscal 2026 came to $6.3 billion, most of it taxes on the buying and selling of securities. Every option sold to a losing trader is a receipt for the treasury as much as a fee for the exchange, and the government collects on the activity its own regulator is trying to curb.

Fewer than one in a hundred Indians trade derivatives today, on a market the regulator is already straining to cool, in a country where hundreds of millions are opening their first investment accounts. A buyer of NSE is wagering that India decides it wants the activity, and the tax it throws off, more than it minds the losses. Every market democracy has faced that choice. South Korea’s index options were once the most heavily traded contract in the world, until in 2012 its regulator made them five times more expensive to curb the speculation, and the boom collapsed. India is facing the same choice at a scale no rich country reached, and among people far poorer.