Distribution Is Still Destiny

India still rewards whoever is easiest to find, easiest to trust and easiest to replenish.

In parts of Uttar Pradesh, the largest Indian state, a single wholesale distributor can reach 50 to 60 villages. Snack maker Balaji has built its factories close to those clusters, keeping the chain between factory and shop as short as possible and it prices things in a way that shopkeepers want to stock the product rather than having to be convinced by a salesperson.

E-commerce accounted for 6% of urban India’s FMCG sales, and up to 14% across all metros, in Q4 2025, with traditional retail doing the rest, and rural volume growth ran at 2.9% against 2.3% in urban areas, the eighth consecutive quarter of outperformance, per NielsenIQ. That gap is being won and lost at the wholesale and distribution layer, by companies that make their products the easiest to find, easiest to trust and easiest to replenish.

"Affordable premium" in rural India is a constrained idea for exactly this reason. The room that exists is to take a brand the consumer already trusts and move it up one price step, Parle-G to butter cookie to cashew cookie, soap bar to liquid dispenser, at the same INR 5, INR 10 or INR 20 they are already comfortable spending. One or two new products, not ten, because the upgrade has to travel through the same shops, carry the same familiar name and ask for roughly the same money.

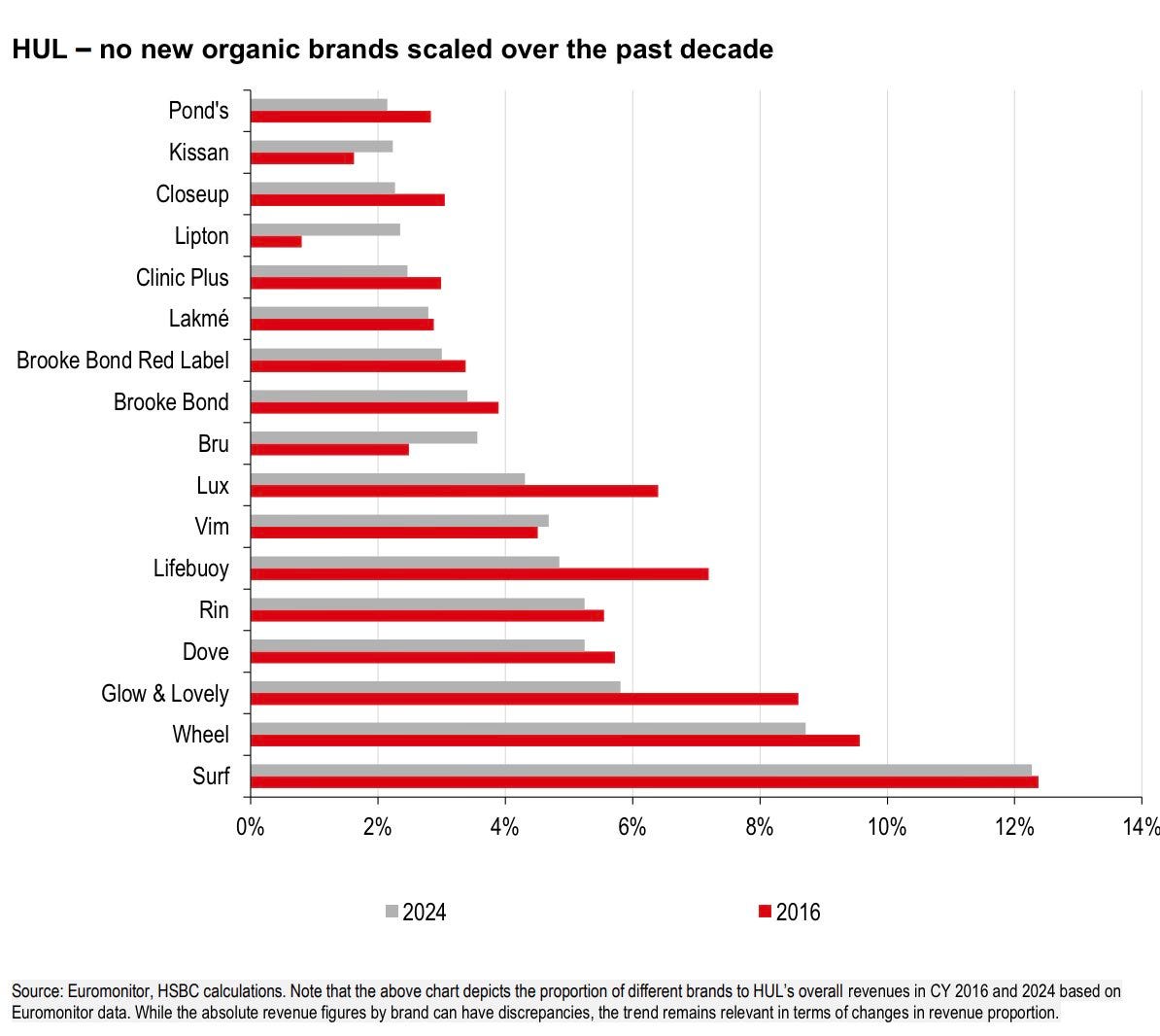

HSBC estimates that 40 to 45% of Hindustan Unilever’s revenues come from what it calls slow-moving segments: tea, soaps, Horlicks and Glow and Lovely, all high-penetration categories with very little upgrade path left, and the company has not built a single new organic brand at scale in a decade. Britannia has had its non-biscuit portfolio stuck at roughly 22 to 25% of revenues for three to four years, and per HSBC, its share of e-commerce including quick commerce is still in the high-single digits. Balaji keeps building new distribution into underpenetrated markets; HUL and Britannia are, in different ways, companies whose existing distribution has run out of road.

Rural distribution means the stockist and the kirana; urban distribution means the telco bundle, the ranking algorithm, the society gate, the dark store, but whoever sits between a product and repeated usage in any of these forms ends up controlling the demand.

Home services platform Urban Company has built its business around a constraint that has no physical shelf. Home services are incident-driven, a broken fan, a blocked drain, a facial before a wedding, and every one of those situations is its own separate demand context. Advertising bathroom cleaning to someone who needs a massage does not work, and running targeted performance ads for appliance repair does not work either because the need does not exist until the appliance breaks, so the company has focused mostly on making sure people have heard of it, not on chasing them.

In value-commerce, who sits closest to the moment of demand has separated Meesho from its rivals more cleanly than product or price. Nearly 199 million people bought something on Meesho over the fiscal year that ended last March, orders grew 36%, and it has cemented its position as the largest free cash flow generator among scaled e-commerce platforms in India.

Its shoppers in smaller cities and towns had come to online shopping through WhatsApp and UPI, starting with INR 100 or INR 200 purchases, spending cautiously, and only moving to platforms with bigger or more expensive selections after several transactions and often more than a year of experience. Meesho got there first, was reliable enough that people came back, and the habit formed.

On Meesho, new products surface quickly, the feed feels fresh, and sellers send more inventory because the fees are simple enough to make the math work. Others run on legacy infrastructure in a way that new, unproven products end up sitting behind ones that have already built up reviews and search history.

Telecom operator Jio has 503 million mobile subscribers; rival Airtel has 349 million, and both, along with cable operators Tata Play and Dish TV, have bundled 20 to 25 streaming services into their existing plans, creating a distribution layer for OTT content that individual apps cannot match on their own.

In smaller cities and towns there are already more people watching OTT content through these bundles than through direct subscriptions, and Airtel’s bundle, which includes Netflix, JioHotstar, Zee5 and SonyLiv among 25 or more platforms, starts at INR 279 a month against a stated standalone value of INR 750. A streaming service that has spent years trying to convince people to sign up directly can be lapped by one that simply gets added to a phone plan the subscriber already pays for.

Payments company PhonePe, used by hundreds of millions of users, did not try to build a full travel booking product but has added a thin layer that lets users book flights or buses without leaving the payments app, enough to capture the transaction, not so much that it weighs down what the app is actually for.

Apartment society software startup Mygate started as a tool for managing visitor entry in gated housing societies, logging who comes and goes and sending residents a notification when a delivery arrives. It turned out that most of the people walking through those gates every day are delivery workers, from Swiggy, Zomato, Blinkit, Flipkart and Amazon. That has made Mygate’s actual user base, the residents of those societies, one of the more precisely targetable audiences in urban India: affluent households with cars, dual incomes and someone ordering delivery almost every day, which is why quick commerce and e-commerce companies have been buying ads on Mygate at scale.

Devotional content platform AppsForBharat found the same thing in a different context. It has built apps for devotional content, bhajans, temple livestreams, religious calendars, and its decision to build more temple and content partnerships in north India created a business concentrated in the north, because users came wherever the supply of relevant content already was. The distribution, not the product, created the geography.

A new air-conditioner brand can price 5% below Voltas and still lose, because someone spending INR 35,000 to INR 40,000 wants to know the company will send a technician if something goes wrong two years later, and that confidence comes from the brand being present in enough stores that it feels established.

LG Electronics India, the market leader across refrigerators, washing machines and inverter air conditioners, runs more than 1,000 service centres staffed by 13,300 certified engineers, supported by 777 brand shops and over 30,000 sub-dealers, and that infrastructure is what a consumer is really buying when they pick LG over a brand they have never had to call.

LG has also launched what it calls an essential series in tier-2 and smaller cities, refrigerators and washing machines at lower price points with basic-plus features, targeting first-time buyers who are aspirational but not yet ready for the flagship range. It is the consumer durables version of Parle-G to butter cookie.

Logistics platform Porter has built its business around a specific kind of customer: the trader or small business owner who needs to move goods across a city on short notice, without knowing in the morning how many vehicles they will need by afternoon. The value is not the truck but in the certainty of having one when the need arrives.

Food delivery platform Zomato’s bestselling categories, biryani and pizza, work because they can survive a 30-minute delivery, fill a meal on their own, and are ordered from enough restaurants that the platform can consistently fulfil the demand. Its rapid-delivery format Bolt failed because restaurants could not cook fast enough to meet the promise. Bistro, Zomato’s office-hours snacking service, works in locations where there are enough office workers nearby, enough delivery riders who are free during the day, and a small company-run kitchen already in a dark store. Take away any one of those and the economics seem to fall apart.

India still rewards whoever is easiest to find, easiest to trust and easiest to replenish. The product question usually comes after.

You mean, tier 2+ India.

The middle class in tier 1 and upper middle class have different approach