Indian EV Startups Have Become 'Uninvestable,' Bernstein Says

India’s electric vehicle revolution is turning into a case study of incumbent advantage with startups becoming “uninvestable,” says investment bank Bernstein.

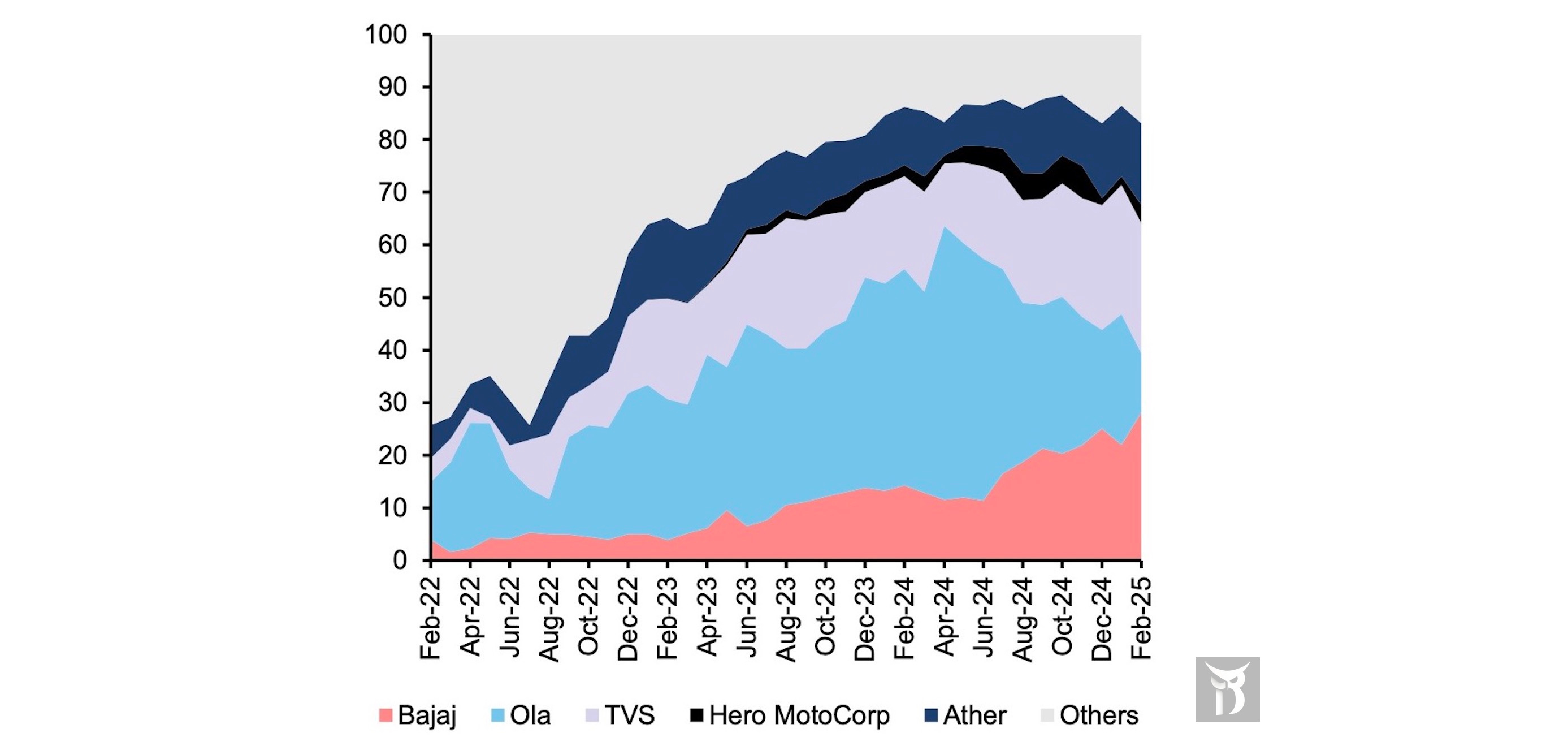

Over 150 startups have mushroomed in India's electric two-wheeler market in recent years, but a rapid consolidation has left just four companies controlling 80% of the segment. Traditional manufacturers Bajaj and TVS now command 50% of the market between them. “Incumbents are becoming relevant in EV 2WS,” said the bank’s report.

An analysis of financial results across the industry reveals just how dramatically fortunes have diverged between traditional manufacturers and their startup challengers. Ola Electric, despite its high profile, reported a negative EBITDA margin of 17.6% in the first half of fiscal year 2025, with net losses of $97.9 million. Competitor Ather, which is looking to go public in the coming quarters, fared even worse with a 37% negative EBITDA margin in FY24 and losses exceeding $122 million. Greaves Electric Mobility posted a 30.3% negative EBITDA margin.

Contrast this with incumbent manufacturers: Bajaj’s entire electric vehicle division reached breakeven in early FY25, while TVS has achieved profitability at the contribution margin level even without accounting for government incentives.

Bernstein says established players — who already lead the gasoline-powered automobile market in India — are making use of their “structural” advantages. Traditional manufacturers have rapidly expanded their distribution networks, with Bajaj growing from just 200 EV stores to approximately 3,250 in under a year. This approaches two-thirds of its traditional combustion engine network of 6,000 outlets. TVS nearly doubled its EV stores to 750, while Ola built out to 4,000 points of presence.

Most startups lack comparable offline distribution capabilities. “By the time these startups manage to scale and establish a solid offline presence, much of the market may have already been claimed,” the Bernstein report states.

Government policy has compounded these challenges. India has progressively reduced its FAME subsidies for electric two-wheelers from ₹50,000-60,000 ($580-700) per vehicle to just ₹10,000 ($117), with further cuts to ₹5,000 expected in April 2025. Simultaneously, the government shifted has support toward production-linked incentives that benefit select manufacturers.

This policy pivot has proven particularly problematic for startups. While Bajaj, TVS, Hero, Ola, Eicher, Mahindra, Piaggio, and Hop Electric qualify for production-linked incentives, most emerging startups do not. Notable exclusions include Ather, Ampere, Revolt, and Ultraviolette. Without these incentives, startups face structural cost disadvantages difficult to overcome.

Incumbents are also further cementing their position with aggressive product plans. TVS is preparing a new affordable scooter brand, Bajaj has launched revamped Chetak variants, and Honda and Suzuki will enter the market in 2025. Honda has even announced plans to establish a dedicated electric motorcycle manufacturing plant by 2028.

Bernstein sees few potential survivors among the startup cohort.

“We predict most of the 150-odd EV two-wheeler startups to see scale-up challenges leading to exits,” the report concludes. “We do not see room for many acquisitions as well, as most lack differentiation.”

The message for investors is unambiguous: avoid being “swayed by lower valuation ask or the allure of trading momentum” when startups seek public market funding. Bernstein maintains that even if some startups reduce losses, this “does not guarantee scalability or justify any valuation.”

Follow India Dispatch on WhatsApp.