The Indian IT Compounding Machine Has Stopped Compounding

Bookings grew 10% in FY26. Revenue grew 2%. Headcount fell. The four assumptions that made the sector a buy for a decade have weakened at the same time, and for the first time.

India’s IT services giants have successfully defended profitability over the last four years, but the model that once made those profits compound is now visibly beginning to fray.

Full-year FY26 operating margins held across the six largest firms, they disclosed in their financials in recent days. Tata Consultancy Services posted its highest margin in four years, and the IT cohort again delivered the cost discipline it has long been known for.

Yet nine of the ten major firms saw their shares fall on the day they reported, and the group is now down 20-30% year to date. Reason? Investors selling the stocks don’t doubt that the firms know how to protect their margins – but are convinced that it’s not the most meaningful metric at the moment.

For most of the past decade or so, the investment case for Indian IT has rested on four assumptions. That bookings convert into revenue at a reasonably predictable rate. Productivity gains create scope for market-share expansion rather than being passed back to clients. Faster growth justifies a valuation premium to global peers. And a diversified client base prevents any one customer, sector or project from disturbing the annual picture wildly.

The first two of those assumptions have broken outright in FY26, the third is now breaking under the weight of top-client concentration, and the last is being contested at the source, since the cohort is still being asked to justify a valuation premium that was built when growth looked very different. That is why a resilient profit performance has still produced a poor share-price response.

TCS contracted 2.4% in constant currency over the year ended March, its first annual revenue decline since going public, while Wipro shrank 1.6% in a third consecutive year of contraction. Tech Mahindra grew by just 0.6%. Infosys grew 3.1% over the full year and HCLTech 3.9%, the only top-five firms to register meaningful gains, and both have widened the bands of their FY27 guidance to absorb slower client decision-making in Western markets and AI-led pricing pressure. None of the six majors produced a positive surprise on both revenue and margin in the March quarter, Jefferies says, the first such reporting cycle in four years.

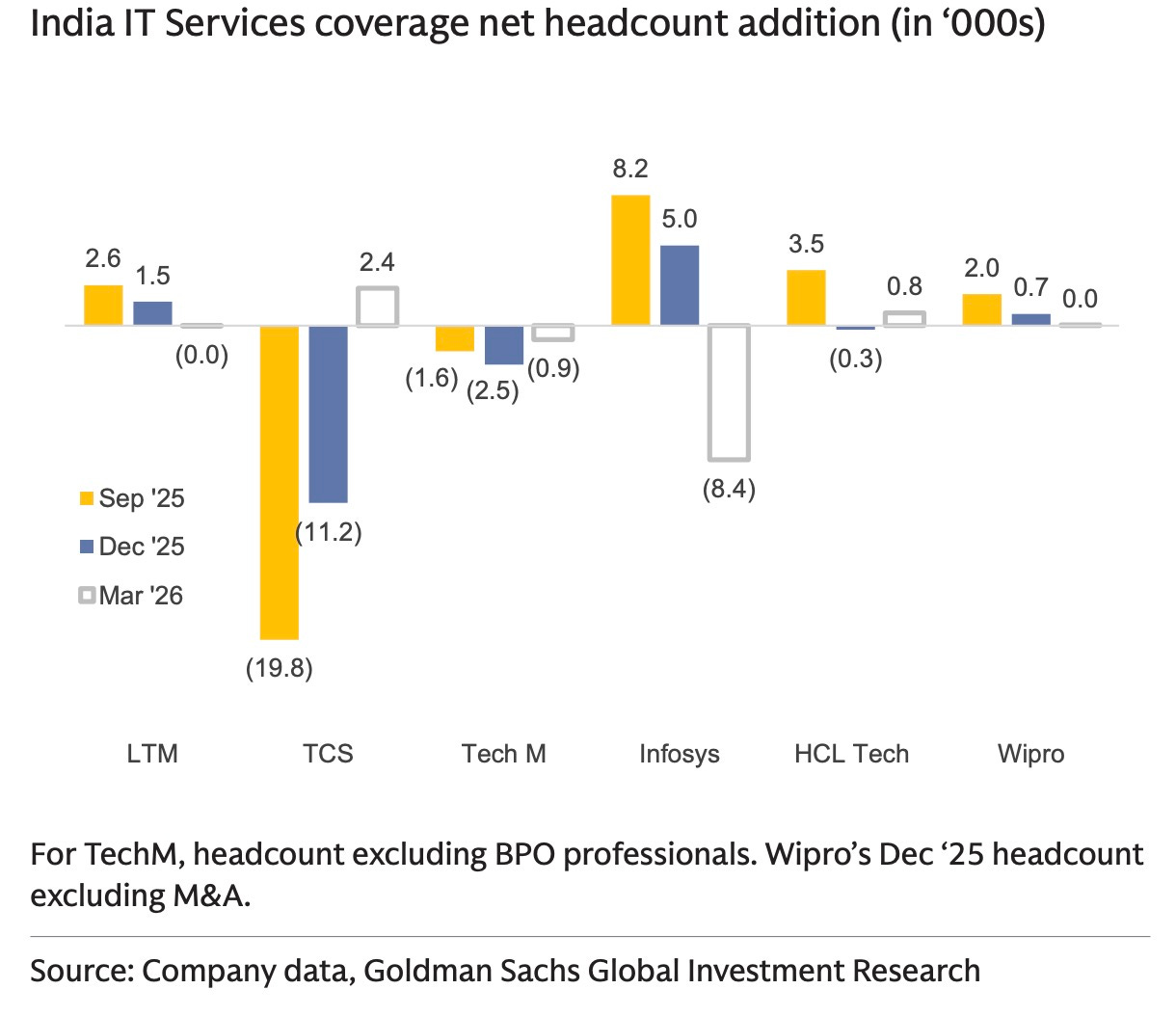

Margins have held despite the revenue disappointment. Net hiring across the top six turned negative at -0.2% for the year, revenue per employee rose across most of the cohort, and EBIT per employee rose with it. Infosys cut 8,400 jobs in the March quarter alone, while TCS reduced its workforce by 3.9% over the full year. In earlier cycles, these numbers would have been read as operating leverage, but the earnings defence in FY26 is being achieved by shrinking the denominator rather than expanding the addressable opportunity.

HCLTech quantified the downstream effect (becoming the first Indian IT giant to do so), calling out 2-3% annual revenue compression from AI productivity gains flowing back to clients. Infosys management said on its earnings call that competitive intensity was forcing productivity gains to be returned rather than retained as margin. UBS estimates that the theoretical ceiling on productivity-driven revenue deflation across legacy service lines may be 25-35% under enterprise-wide AI deployment, though realised gains over the medium term are more likely to settle around 10-20%. Even the lower end of that range is large enough to matter in an industry whose economics were built on utilisation, offshore labour pools and steady additions to billable headcount.

The Indian cohort remains roughly half time-and-materials and half fixed-price, a mix that leaves providers exposed when automation reduces the effort required to perform the same task. At that balance, UBS reckons a 30% productivity gain can wipe out essentially all operating margin unless the firm replaces the lost billable effort with new revenue at scale. A higher fixed-price share lets the provider retain more of the gain. Infosys has moved from 40% fixed-price work in FY13 to 55% in FY25, and Accenture sits at roughly 60%. Twelve years into this transition, however, the average Indian large-cap contract base still sits close to an even split.

If automation enables a provider to deliver the same service with fewer people while holding price, margins expand. If the client demands that the saving be reflected in the contract, revenue compresses. And if competitors reprice aggressively to protect volumes, the gain leaks away before it meets the income statement. FY26 has increasingly placed Indian IT firms in the second and third of those worlds.

Aggregate deal wins across the top six grew 10% in FY26, while aggregate dollar revenue grew only 2%, and the gap widened as the year progressed. Infosys signed $3.2 billion of large deals in the March quarter, a 23% year-on-year increase in total contract value, yet revenue in the same period contracted 1.3% sequentially in constant currency. Net new deal wins at Infosys ran 40% above the year-ago period over the first nine months of FY26, and the equivalent figure at HCLTech was 21%, but neither firm has converted those wins into reported revenue at a pace that matches prior cycles.

Clients are still signing contracts, but they are taking longer to start, ramping more slowly once they do, embedding productivity clauses from the outset, cutting discretionary scope and cancelling or delaying projects whose economics have become uncertain in the light of AI, hardware constraints or macro caution. The industry conversation has moved from pipelines and total contract value to ramp delays, suspended work and signed deals that do not behave like revenue.

HCLTech and Tech Mahindra each flagged discretionary cuts at two U.S. telecom clients. HCLTech also disclosed the suspension of two SAP ECC migration projects, one at a manufacturing client and one at a retailer, both seemingly betting that SAP will postpone its support deadline rather than force an immediate capital commitment. Wipro’s weakness in banking and financial services was tied to specific accounts, and Infosys attributed 75-100 basis points of its FY27 growth headwind to softer spending and a partial contract loss at Daimler. At least one major reported a delayed contract ramp-up caused not by its own execution but by a client’s hardware supply problem.

Top-five client revenue across the large Indian IT firms grew just 1% in FY26, compared with 8% the previous year. Stripping out HCLTech, which added a major new client to its top five in FY25, growth across the rest of the cohort was zero. Over the past decade, top-client revenue growth and overall IT-services revenue growth moved with an 81% correlation, but that relationship decoupled this year. Consensus revenue forecasts, surveyed by Jefferies, for the cohort’s largest enterprise clients have been revised up by 1.8-2.2% over the past three months for CY26 and CY27, even as the IT-services firms serving those clients have seen no equivalent improvement in their own numbers.

Hardware has risen from 31% of enterprise IT budgets in 2023 to 36% in 2025, putting it on course to move past the previous peak of 39% set in 2013. The funding has come almost entirely from the IT services line, which has dropped from 39% of enterprise IT spend in 2022 to a forecast 29% in 2027. AI workloads require GPUs, storage and networking equipment before they require large consulting teams, and the money that might have flowed to Indian IT firms two years ago is now being absorbed by Nvidia, Dell and Cisco. Services demand is not collapsing so much as being reprioritised, leaving discretionary transformation work competing with infrastructure spend in a way it did not during the cloud migration boom.

Infosys said clients are prioritising productivity, automation and platform-led modernisation over growth-led transformation programmes. TCS described spending sentiment as cautious in banking, financial services, insurance and manufacturing. Cognizant, Accenture and Capgemini are guiding to low-single-digit growth on broadly the same enterprise dynamic. The constraint is not so much Indian firms losing share to Western peers as the pool of discretionary services spending itself shrinking, and Indian IT is especially exposed to that pool. BFSI, retail and manufacturing account for much of cohort revenue, and each segment contracted sequentially at Infosys in the March quarter.

Several majors are walking away from low-value or intensely competitive traditional contracts to protect long-run mix. Legacy work is being repriced, automated or exited before AI-native, outcome-linked and platform-led revenue is large enough to fill the gap.

Deloitte has rolled out Anthropic’s Claude to roughly 470,000 employees, supported by a dedicated Claude Center of Excellence. Cognizant has deployed Claude across roughly 350,000 employees and integrated it into its Agent Foundry modernisation platform. Accenture has trained roughly 30,000 professionals on Claude and Claude Code and runs a dedicated Anthropic Business Group. No Indian IT major has disclosed a Claude or equivalent deployment at comparable workforce scale, even as the Indian firms compete for the same enterprise transformation work and pitch to the same buyers with similar language around automation, agents and modernisation.

OpenAI’s Frontier Alliances launched in February with Accenture, Capgemini, McKinsey and BCG as founding members. Anthropic’s Claude Partner Network launched in March with a $100 million partner fund, and its four named anchor partners are Accenture, Deloitte, Infosys and Cognizant. Wipro, HCLTech, Tech Mahindra and LTIMindtree sit in Anthropic’s second-tier, model-agnostic partner bucket, and TCS is listed as pending in the same tier. Infosys is the only one of the six Indian IT majors in the top tier of either architecture. These alliances provide a route into Services-as-Software offerings where revenue is tied to AI agents, intellectual property and repeatable platforms rather than to people billing by the hour.

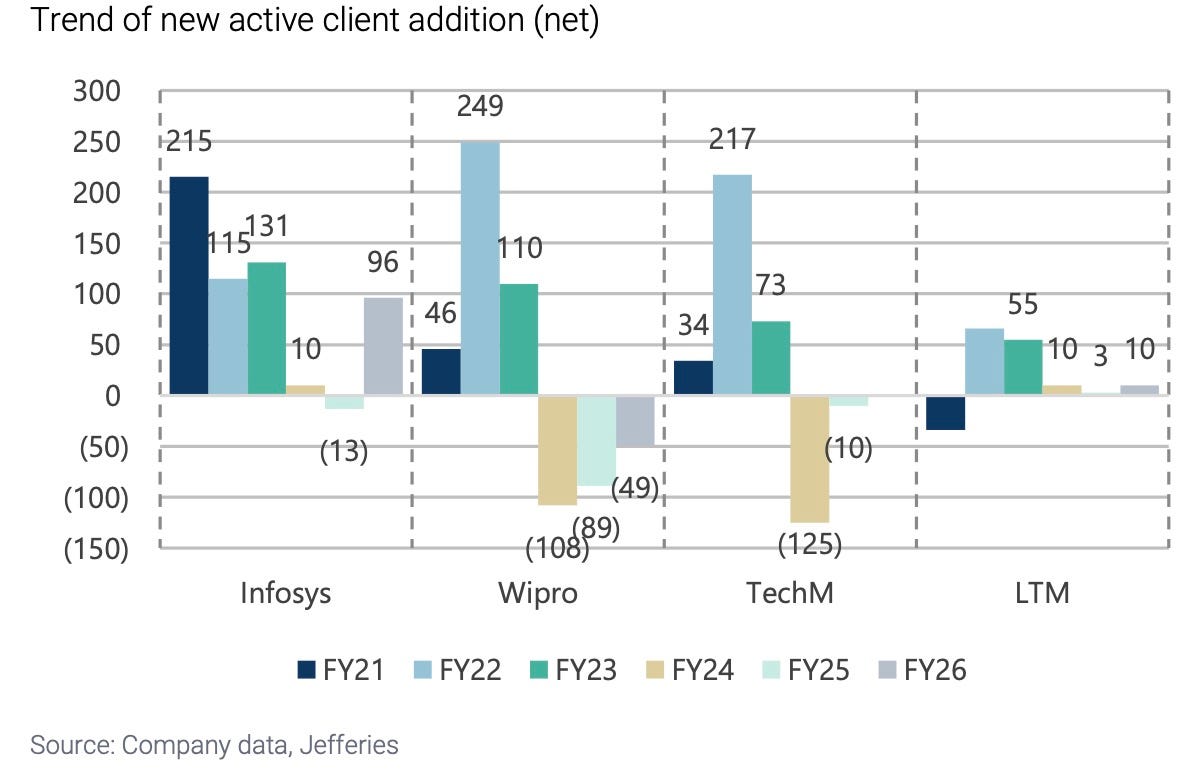

The growth wave of FY21-23 came from new logo additions during the COVID-era rush into cloud, when Infosys, Wipro, Tech Mahindra and LTIMindtree each added net new clients in the high tens to low hundreds. In FY26, net new logo additions across the same four firms were flat to negative, meaning the top accounts have stopped growing just as the new-logo engine has stopped replenishing the base. During the second phase of the cloud transition, Indian IT firms de-rated roughly 20% over two years before re-rating 35-40% over the following two years, and the re-rating came ahead of the recovery in reported revenue growth because investors saw three to four quarters of digital-revenue disclosures that proved replacement business was scaling. The equivalent evidence for AI has not yet arrived.

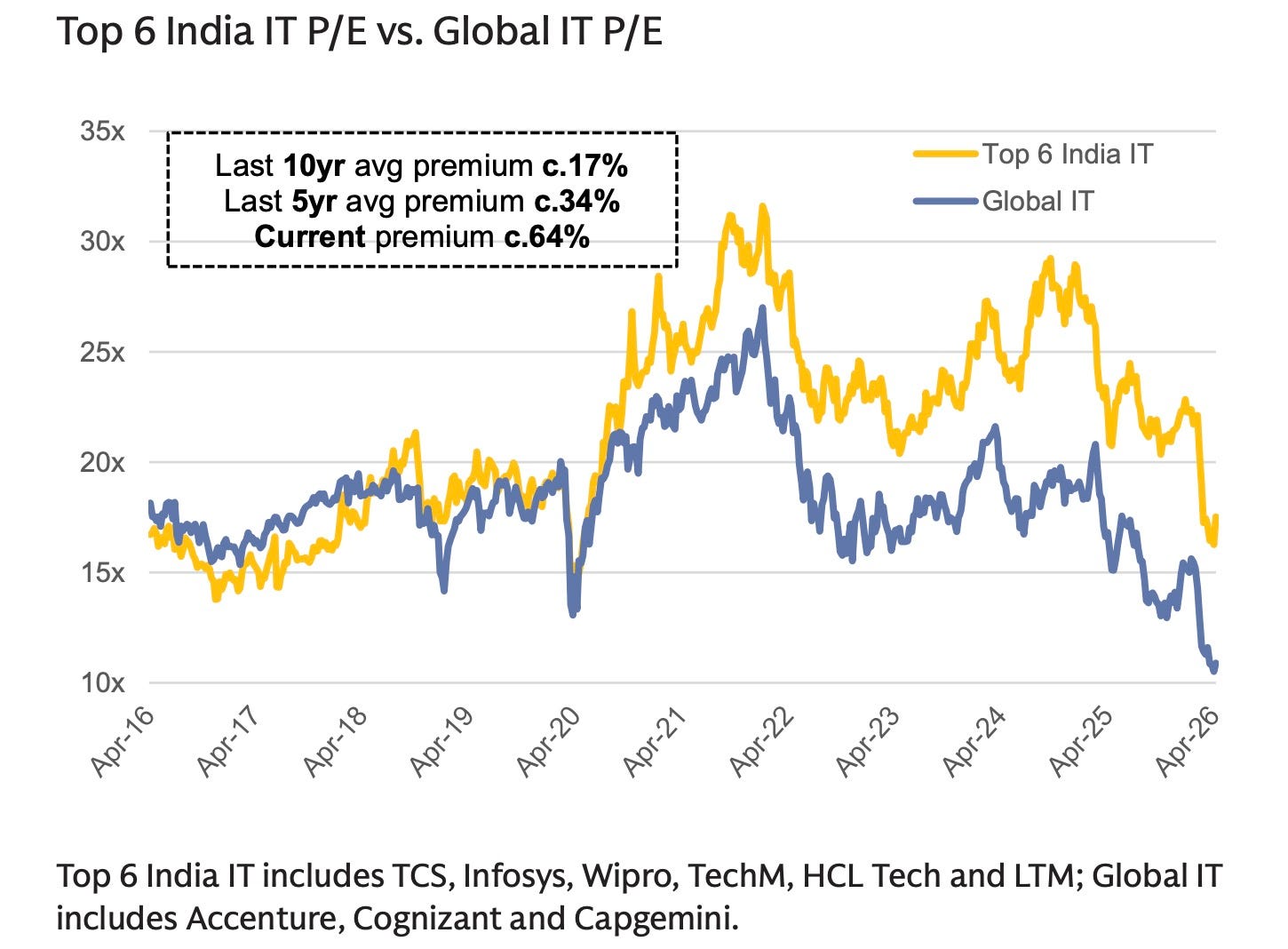

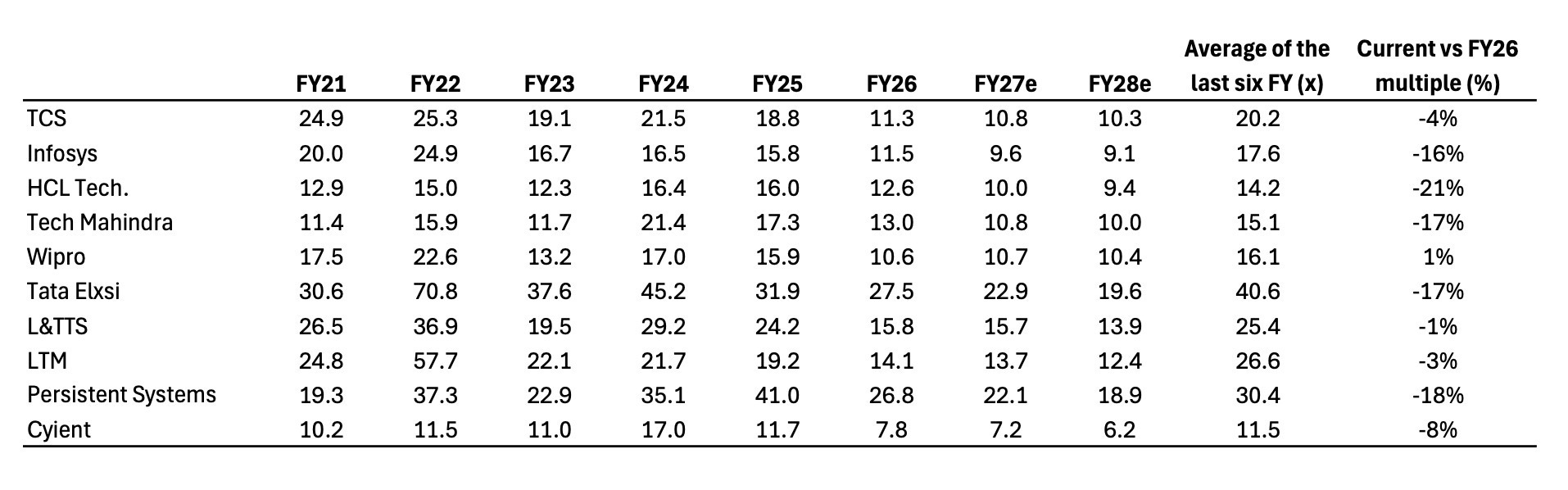

The top five Indian IT firms still trade at a 30% price-to-earnings premium to Accenture, against a ten-year average discount of 11% and a five-year average discount of 3%. Across the top six Indian firms, the premium to Accenture, Cognizant and Capgemini is near 64%, compared with a ten-year average of 17%, even though both cohorts are guiding to low-single-digit growth for the coming year. Infosys’s FY27 constant-currency revenue guidance of 1.5-3.5% implies an average sequential growth rate broadly aligned with U.S.-listed peers, and the valuation gap is hard to justify on growth alone.

Nifty IT trades at 17 times forward earnings, broadly in line with the 2015-19 pre-COVID average and well below the 2021-25 average of 25 times. The index now trades at an 8% discount to the broader Nifty 50, compared with a ten-year average premium of 14%, and EV/EBITDA multiples across the cohort sit roughly 30-45% below their six-year averages. The numbers price in some cyclical disappointment but do not settle whether the sector is digesting a weak spending cycle or entering a more difficult business-model transition.

Indian IT has yet to show that AI can generate billable platforms, agents, managed services and outcome-linked work faster than it compresses the legacy services book. It needs to move more of its contract base towards fixed-price and outcome structures, own more of the automation layer, and grow revenue per employee faster than productivity gains are handed back to clients through pricing. Persistent and Coforge have grown revenue per employee by 21-34% over three years, against 13-16% at the strongest large caps and flat or negative figures at the weakest.

Indian IT has certainly not lost its ability to manage costs, and it has not become irrelevant to global enterprises. But the old compounding formula has weakened. The industry now has to prove it can grow without adding people, keep productivity gains without surrendering them to clients, and turn AI partnerships into revenue rather than announcements. Until then, the street appears fixated on treating margins as evidence of discipline, but not evidence of a moat.

Cost control can buy time, but it cannot replace demand forever. The next few years will probably depend on whether these firms can create new revenue streams without relying on headcount growth. One thing I kept wondering while reading this was whether Indian IT firms are structurally late to the AI transition, or if the market is underestimating how quickly they can adapt once enterprise spending stabilizes. You mentioned partnerships and platform-led revenue, but I’m curious what concrete signals you would watch for over the next 12 to 18 months that would convince you the sector has actually found a new compounding engine rather than just defending margins during a slowdown.

very well written Manish!