India’s Banks Grapple With Liquidity Constraints as Growth Slows

India’s banks are grappling with some of the world’s tightest cash reserve requirements, according to HSBC, a regulatory burden that is hindering their ability to lend and support economic growth. These strict rules, which exceed those in the US, Middle East, and Southeast Asia, come at a time when India is already facing a slowdown in its economy and emerging stress in consumer credit markets.

Banks in India must comply with multiple reserve ratios including the cash reserve ratio, the statutory liquidity ratio, the liquidity coverage ratio, and the net stable funding ratio. “Compared to this, banks in other geographies like ASEAN economies, the US and the Middle East primarily follow the LCR/NSFR and a lower overall reserve requirement,” HSBC analysts wrote in a report.

The strict rules come as signs emerge of stress in India’s consumer credit markets, particularly in microfinance, unsecured personal loans and credit cards. However, HSBC argues that unlike previous credit cycles, banks now have stronger capital buffers and provisions to absorb potential losses.

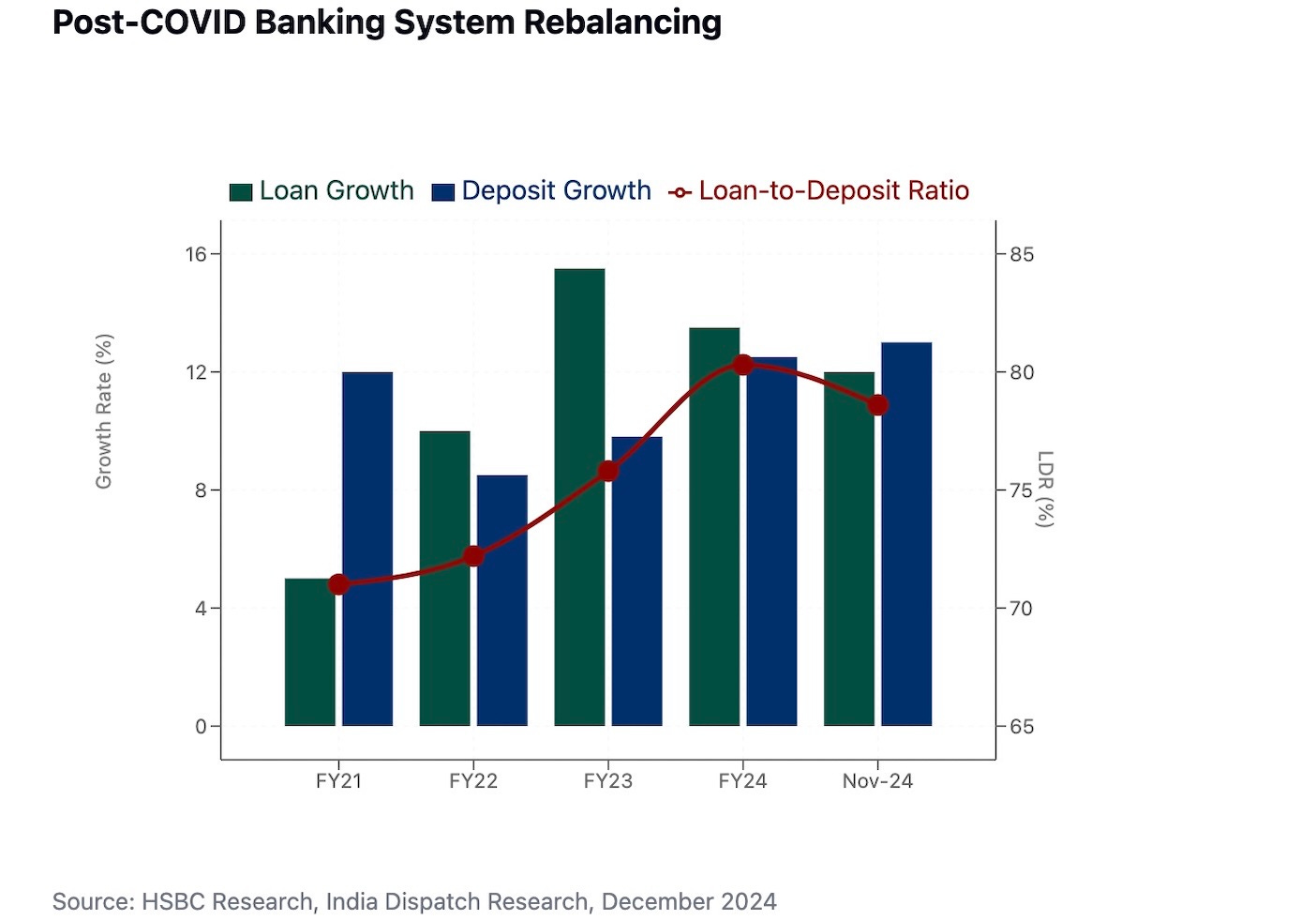

The research highlights how post-pandemic excesses in India’s financial system “stand corrected,” including a normalization of loan-to-deposit ratios and reduction in what HSBC terms “excessive growth in unsecured loans”.

But the high reserve requirements are constraining banks’ ability to lend, with HSBC calculating that every 100 basis point cut in reserves could boost loan and deposit growth rates by 250 basis points. These resources could be directed to sectors with wider economic impact like housing, small businesses and infrastructure. The Reserve Bank of India is in the process of considering extending the guidelines on the cap on foreclosure charges and prepayment penalties on loans to micro and small enterprises.

The findings underscore the balancing act facing Indian regulators as they seek to contain consumer credit risks while ensuring sufficient lending to support economic growth, which HSBC forecasts will moderate to 5.4% in FY25 from the Reserve Bank of India’s previous estimate of 7.2%.

HSBC estimates that at current reserve levels, Indian banks can lend out a lower proportion of their deposits compared to overseas peers. The analysts argue this creates space for regulators to ease liquidity conditions in 2025, which should aid deposit growth.