The Law of Diminishing Points

Large credit card issuers in India are cutting points, capping redemption and spend-gating the lounge.

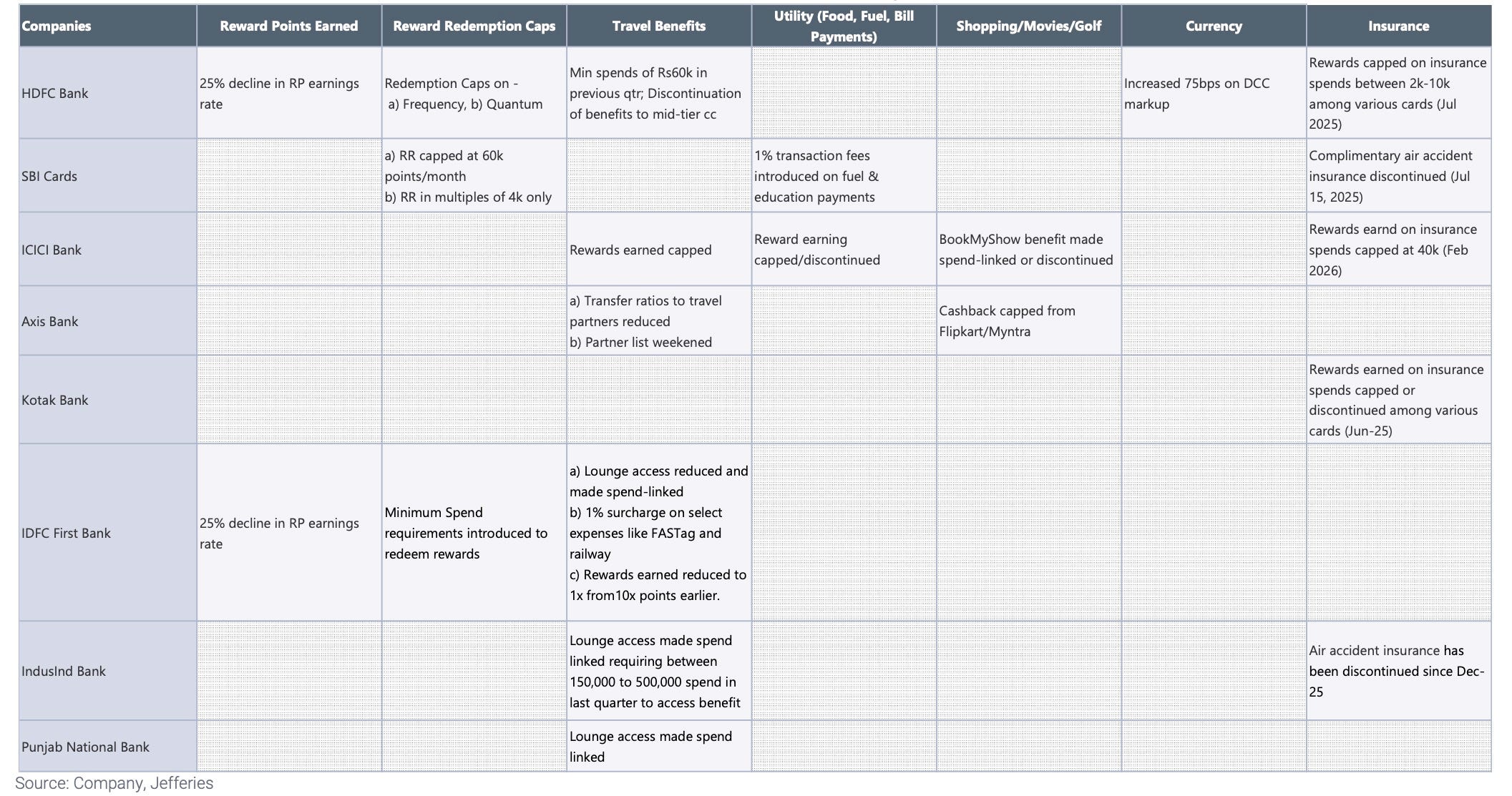

Indian credit cards, offered by largest banks and other top issuers, are quietly getting worse. Since November, paying school fees through a third-party app on an SBI-issued card has cost 1% extra. Its Air India co-brands have earned two-thirds less since March last year, the accident cover that came free is no longer around and reward redemption has been capped.

It has company. Per Jefferies, leading issuers in India have cut reward points, capped redemption, raised spend thresholds, added fees on utility payments, trimmed perks from insurance to travel and made lounge benefits conditional. Conditional means the lounge is free once you’ve kind of paid for it. HDFC Bank has cut reward-point earning rates by 25%, and from July its Regalia Gold requires a minimum quarterly spend for domestic lounge access. IDFC First has cut its earning rates too and tied lounge access to spend.

DreamFolks, the middleman that got cardholders through lounge doors on the banks’ behalf, shut its domestic lounge business last September after Axis Bank and ICICI Bank pulled their offerings.

There’s a very strong reason why banks and other credit card issuers have been forced to pare their offerings.

Rewards get paid out of what the card charges, and the card charges about 1.6% a transaction, against 0.4% on debit. But as UPI eats into plastic card’s transactions – including in the credit card universe, with RuPay – the reward earned by the card has become next to zero.

New Delhi set the merchant fee on UPI at nothing by statute in January 2020, which leaves the card competing on price with a rival that is legally barred from charging anything.

UPI moved about $3.3 trillion in the fiscal year that ended in March. Credit cards did about $250 billion, during the same period and card spend growth has stepped down from 27% in FY24 to roughly 15% in FY25 to 12% in FY26.

The interest payers are thinning out, too. SBI Cards’ revolver mix, the share that carries a balance instead of settling in full, has slid from 28% in FY21 to 22% in FY26, a trend its management calls “a downward bias.” Transactors, who settle in full, collect the points and pay no interest, are now 46% of the mix. Reward costs for the industry climbed back to 28bp of credit-card transaction value in FY25, which works out to 0.28% of everything put on cards. Set that against the 1.6% the card charges and the giveaway is eating roughly a sixth of the headline rate.

To be sure, this is perks rationing, not a consumer-finance collapse. Credit cards remain a profitable acquisition tool for banks, and Jefferies has them at 8% of HDFC Bank’s PAT, 7% at ICICI Bank, 9% at Axis and 4% at Kotak, which is the sort of profit pool you trim perks to protect.

The squeeze appears specific to the traditional model that needed/enjoyed the fat margin, where the 1.6% charge and a deep pool of revolvers paid for the points, the plastic and the lounge. RuPay credit cards, the only ones allowed on UPI’s QR rails, run on transactions averaging about $12, most of them below the level where any merchant fee applies at all. Their users tap roughly eight times as often as traditional cardholders. It is credit built for thin margins, on rails someone else already paid for.