How Big is India's E-commerce Market? Don't Ask Bain.

Bain has been updating its answer since 2020. The answer keeps getting smaller.

India’s online shopping market is very hard to forecast. It has 1.4 billion people, spread across income levels, languages and infrastructure realities that vary vastly between regions. Its total retail market is worth somewhere around $1 trillion — and the vast majority of it still flows through neighbourhood kirana stores and unorganised traders. Moreover, New Delhi tends to intervene in markets quickly and often unpredictably. Bain & Company, which has been publishing an annual report on this market since 2020, has had to contend with all of that.

It has also had to contend with being consistently wrong about the size of the market.

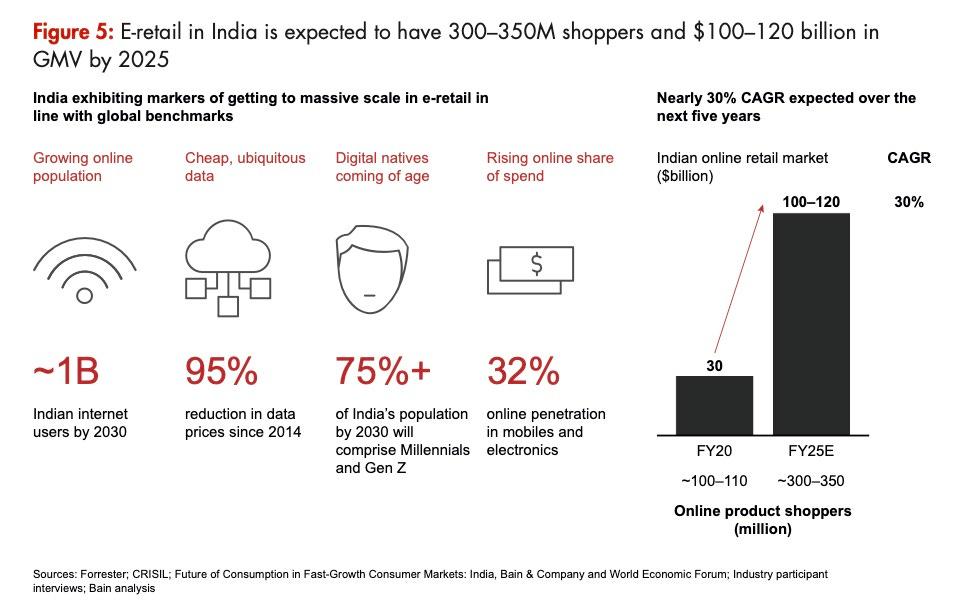

The 2020 report (PDF) opened with this number:

The Indian e-retail market is primed to reach nearly 300 to 350 million shoppers over the next five years—propelling the online Gross Merchandise Value (GMV) to $100 to 120 billion by 2025.

Calendar year 2025, per Bain’s own 2026 report, ended at $65-66 billion. This week’s report does not acknowledge the forecast made six years ago.

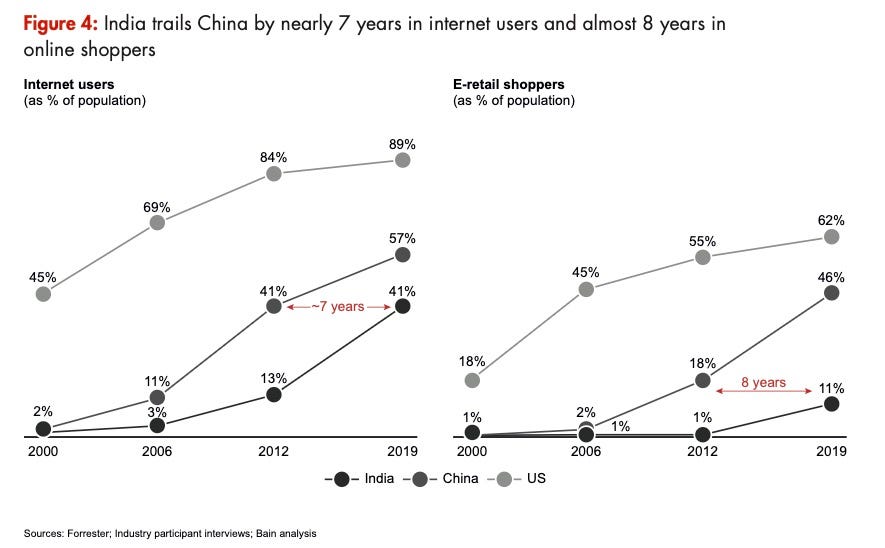

The intellectual foundation of the series is a comparison to China. In 2020, Bain argued that India’s e-retail market looked a lot like China’s had about eight years earlier — before Alibaba and JD.com and cheap smartphones turned it into the world’s largest online shopping market. Data prices in India had just crashed in the same way. Internet users were multiplying rapidly. So the analogy was not unreasonable.

Except, China’s e-retail market was approximately $1.2 trillion in 2019. But despite all the learnings, the 2026 report continues to use China as its primary benchmark.

Each edition also names the disruptions that will define the next chapter of Indian e-commerce. Some of what Bain got wrong here, to be fair, was genuinely unforeseeable.

In 2020, Bain was excited about voice and vernacular — the idea that India’s next hundred million shoppers would arrive not through typed searches but through apps in Hindi, Tamil and Telugu. Back during those days, Google India was reporting 270% year-on-year growth in voice search, and three platforms had each crossed 50 million users:

Several vernacular apps like ShareChat, TikTok and Helo have garnered upwards of 50 million users each.

Shortly after Bain published its maiden India e-commerce report, the Indian government banned TikTok and Helo. BulBul.tv, an Indian live video shopping startup that the same report identified as an emerging model, has since shut down.

The 2021 report cited a second live commerce startup, Simsim, as evidence the model was taking hold in India, describing “9-10x growth in user base over the last year.” Simsim was acquired by YouTube in 2021 and shut down by 2022 — a sad detail worth noting given that even a platform with YouTube’s distribution and resources could not make live commerce work in India.

The 2021 report described voice and vernacular as “vital to win new shoppers.” The 2022 report cited “5x growth in voice-search users and 3x growth in vernacular-search users over the past year.” The 2023 report said “about 25%-30% of first-time shoppers used these offerings.”

The 2025 (PDF) and 2026 reports skip voice and vernacular.

Social commerce got the series’ most precisely quantified forecast. The model Bain had in mind was Pinduoduo, a Chinese platform that built hundreds of millions of users by letting people bargain in groups and rope in friends for discounts. India’s demographics seemed to suit it: young, price-sensitive, deeply networked, spending hours daily on social media. From the 2021 report:

Social commerce GMV (approximately $1.5-2 billion in FY20) could grow at a 55%-60% compound annual growth rate over FY20-25, with the potential to empower 40 million small businesses and turbocharge women entrepreneurs.

At those growth rates, the 2025 social commerce market should have been somewhere between $13 billion and $21 billion.

The 2025 and 2026 reports do not mention social commerce.

The 2021 report also made a prediction that has received less attention than it probably deserves. E-retail, it said, would outgrow India’s modern trade sector — the organised offline retail industry of supermarkets, hypermarket chains and branded stores — by FY26. Modern trade in India is estimated at somewhere around $60-80 billion, a relatively small slice of the total retail market given how much Indian retail still runs through unorganised neighbourhood stores. India’s e-retail market in 2026 will land at somewhere around $78-80 billion. Bain got this right.

Brand aggregators — firms that acquire and scale digitally-native consumer brands, a model that briefly swept global e-commerce on the back of the Thrasio playbook in the U.S. — made their debut in the 2022 report. “Brand aggregators are helping turbocharge these brands,” it said, devoting a section to the model and its potential in India. By 2023, Thrasio had filed for bankruptcy in the U.S. and Indian aggregators were facing similar headwinds. The 2023 report does not mention brand aggregators, and neither do any subsequent editions.

ONDC — the Indian government’s attempt to build open plumbing for e-commerce, modelled on how UPI created a shared payments infrastructure that transformed digital transactions in India — made its debut in the 2022 report:

ONDC aims to create an interoperable network for digital commerce akin to Unified Payment Interface (UPI) network for payments. Although a nascent initiative, its successful and full-scale execution could provide a fillip to the Indian e-retail ecosystem.

ONDC has since struggled to gain meaningful traction, both in the real world and in recent Bain reports.

Quick commerce is where the story runs differently. The model — ordering groceries or household essentials on your phone and receiving them in under ten minutes, from a small warehouse tucked into your neighbourhood — looked shaky in 2022. Global players were burning cash, and Bain was measured:

Long-term sustainability of the model (especially <15-minute model) is unproven, especially in the absence of delivery and/or convenience fees.

In India’s largest cities, it turned out to work. Blinkit, Zepto, Instamart and Flipkart Minutes have become part of the daily texture of urban life in Mumbai, Delhi and Bengaluru in a way that quick commerce has managed almost nowhere else in the world. Bain is now declaring India as having “emerged at the forefront of Q-commerce globally,” projecting the market at $65-70 billion by 2030 — roughly equal to the entire current e-retail market.

In the 2025 report, hyper-value commerce — very cheap goods sold through platforms targeting price-sensitive shoppers in smaller Indian cities — was named as one of three forces reshaping Indian e-retail, having grown from 5% of e-retail GMV in 2021 to more than 12% in 2024. The 2025 report cited Temu’s rapid rise in the U.S. as the global template for the model. Temu is now facing severe U.S. tariff exposure following the elimination of the de minimis exemption and has begun pulling back significantly from the American market. In Bain’s new report, hyper-value commerce does not make a cameo. Its place in the framework is taken by conversational commerce, AI assistants reshaping how people discover and buy products online.

To be sure, Bain has raised some concerns over the years. The 2025 report contained a reality check that sat awkwardly alongside its optimistic recovery forecast. Right next to its projections for resumed e-retail growth, it noted that female real earnings in India were approximately 20% lower in FY24 compared to pre-Covid levels, with male real earnings about 3% lower. These are the people the market needs to convert into online shoppers spending more per order.

From the beginning, Bain has also cautioned that India needs a higher per capita GDP for much of the e-commerce story to fly. The $4,000 GDP per capita inflection point is the series’ most reliably rediscovered insight. The argument is that when a country’s average income crosses roughly $4,000 a year, online discretionary spending accelerates sharply — a pattern observed in China and Indonesia that India is expected to replicate around or by 2030.

Bain’s forecasts for India’s e-commerce market, in sequence:

2020: $100-120 billion by 2025. Actual: $65-66 billion.

2021: $120-140 billion by 2026. At Bain’s own new projected growth rate of more than 20% annually, 2026 will land well short of that range.

2022: $150-170 billion by 2027.

2023: $160 billion or more by 2028.

2025: $170-190 billion by 2030.

2026: $170-180 billion by 2030.

Nobody knows whether Indian e-retail can sustain the new projected growth rate and the market has surprised forecasters before. The earlier targets, though, have all passed without being reached, and each time one has, Bain has moved the horizon forward without acknowledging the miss.

Very interesting. Every time I see these reports forecasting high growth over the next 3 / 5 / x years, I always wonder why no one ever looks at past reports to verify how accurate they turned out to be - so thank you for sharing this analysis!

Also, a few thoughts:

1. Using China as a benchmark or leading indicator for India is looking less and less accurate as time goes by. China's market size across categories is in a genuinely different league altogether:

- Online food delivery annual transacting users: 100M at best in India, while China's largest OFD player Meituan has 770M ATUs across verticals; so safely at least 600M overall in China (6X)

- McDonald's outlets: 757 in India vs 7,740 in China (10X)

- Starbucks outlets: 504 in India vs 8,000+ in China (16X, and this is when Starbucks has struggled in China - Luckin Coffee has 30,000 stores)

- Luxury car sales: 50K in India vs BMW, Mercedes & Audi alone at 1.8M in China (36X, and this is after these 3 players have seen multi-year declines, with Chinese brands gaining popularity)

Analysts don't say that India will eventually match China's market sizes on QSRs / cafes / cars / etc, so I wonder why we keep making this comparison for eCommerce. The fact is, China has created a massive middle class, which India hasn't, and hence not only are their B2C categories much bigger, but also India won't see a similar trajectory unless our middle class grows as well.

2. This and other eCommerce reports seem to suggest that what's holding back the next 100 - 200M consumers from shopping online is a lack of access / knowledge / language understanding / trust in online shopping / etc - and hence tech solves to improve supply or reduce friction will be the big unlock. I don't think this is completely true - income growth is likely the real bottleneck for all commerce growth, whether online or offline.

3. Growth has already slowed for legacy eCommerce players, and a lot of current eCommerce growth is being driven by Quick Commerce, which is in turn at least partly led by channel shifts from GT and MT. So even the current CAGR of 21-22% assumed over 2025-30 might just turn out to be slightly optimistic, if you ask me. 45-50% of incremental GMV is expected to come from Quick Commerce, per the report - so if this engine also eventually moderates, I'm not sure what else will drive significant eCommerce growth.

Of course, income growth may surprise on the upside, which will lift all boats - but at present, that's an imponderable.

Great post Manish. So much business analysis is based on "expert" reports like these Bain forecasts. Often they turn out to be way off the mark but no-one seems to bother. Big consultants, data companies and academic institutions still keep churning the PR mill.